Nexus Data #002 - RWA

Intro

Welcome to the second edition of Nexus Data Labs. We’re here to tell stories about onchain data. Our aim is to alert you to what really matters in the fast-developing world of onchain finance.

Thank you to Borja Neira, Frederick Hopkins, Diego Cabral, and Meta for contributing to this issue.

Setting the Scene

Real-World Assets (RWAs) continue to transform from a niche crypto experiment to a key area of focus for traditional finance.

With institutions deepening their RWA offerings — from asset managers tokenizing treasuries to investment banks exploring private credit rails — tokenized assets have become a barometer for traditional finance’s adoption of blockchains.

The direction is clear: the question is no longer if assets will move onchain, but which assets, when, and, subtly, what the underlying ownership and legal architecture actually looks like.

This week’s edition highlights three dimensions of the RWA landscape making headlines: the growing adoption of Tokenized Gold, the expanding market for Tokenized Stocks and US Treasuries, and the challenging integration of RWAs within DeFi protocols.

RWA Overview

Borja Neira | Website | Dashboard

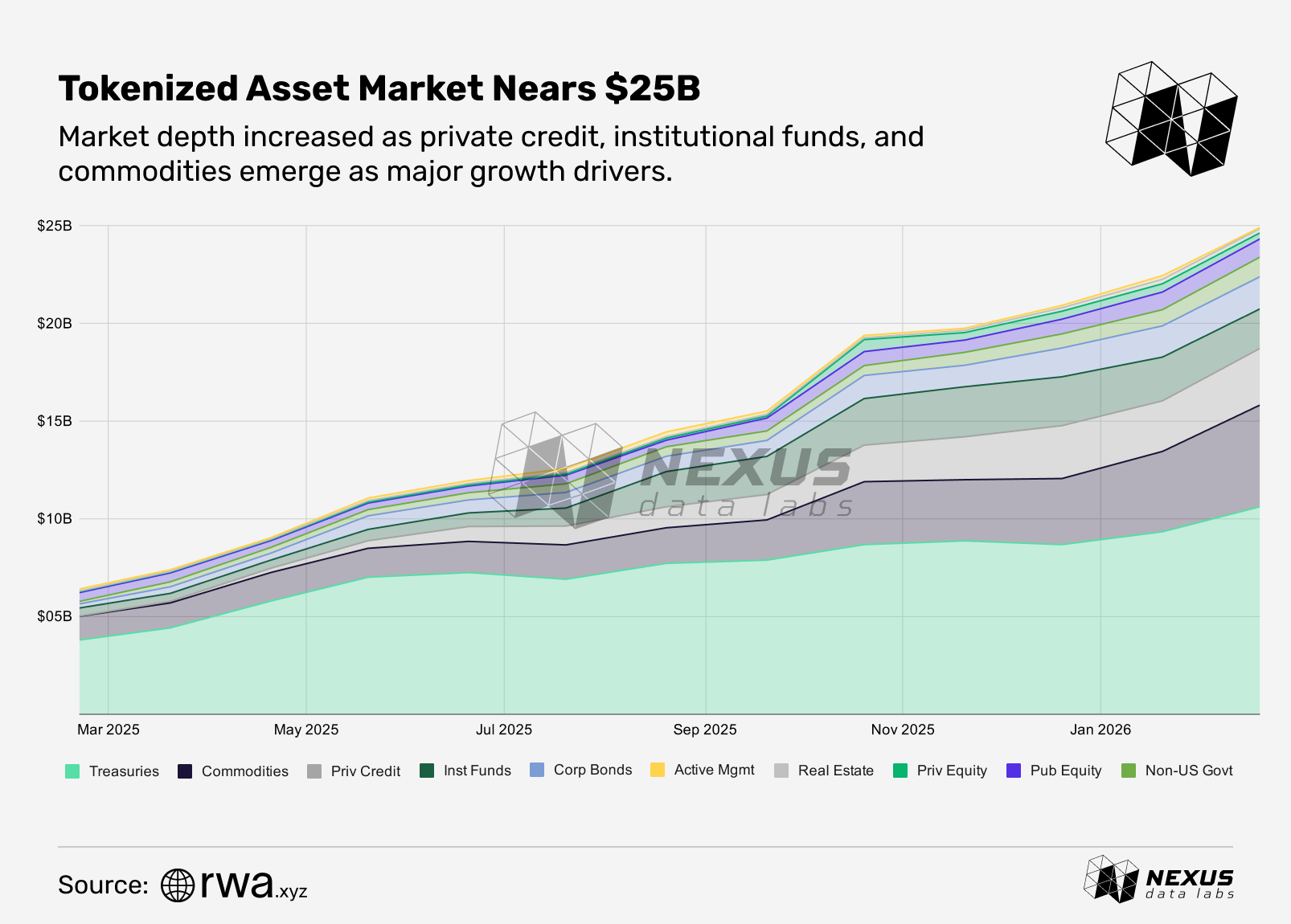

Tokenized assets hit $24.9B, up 289% year-over-year, as six sectors cross $1B

Tokenized assets (excluding stablecoins) reached $24.9B as of Feb. 19, 2026 — nearly 4x from $6.4B a year prior (+$18.5B, +289%). U.S. Treasuries and commodities drove 58% of year-over-year growth, adding $6.8B and $4.0B respectively.

The defining shift was breadth: asset classes exceeding $1B grew from two to six, with private credit ($2.9B), institutional funds ($2.0B), corporate bonds ($1.7B), and non-U.S. government debt ($1.0B) all crossing the threshold — collectively contributing 37% of total growth. Treasury market share declined from 59% to 43%, signaling a more diversified market.

Tokenized US Treasuries

Borja Neira | Website | Dashboard

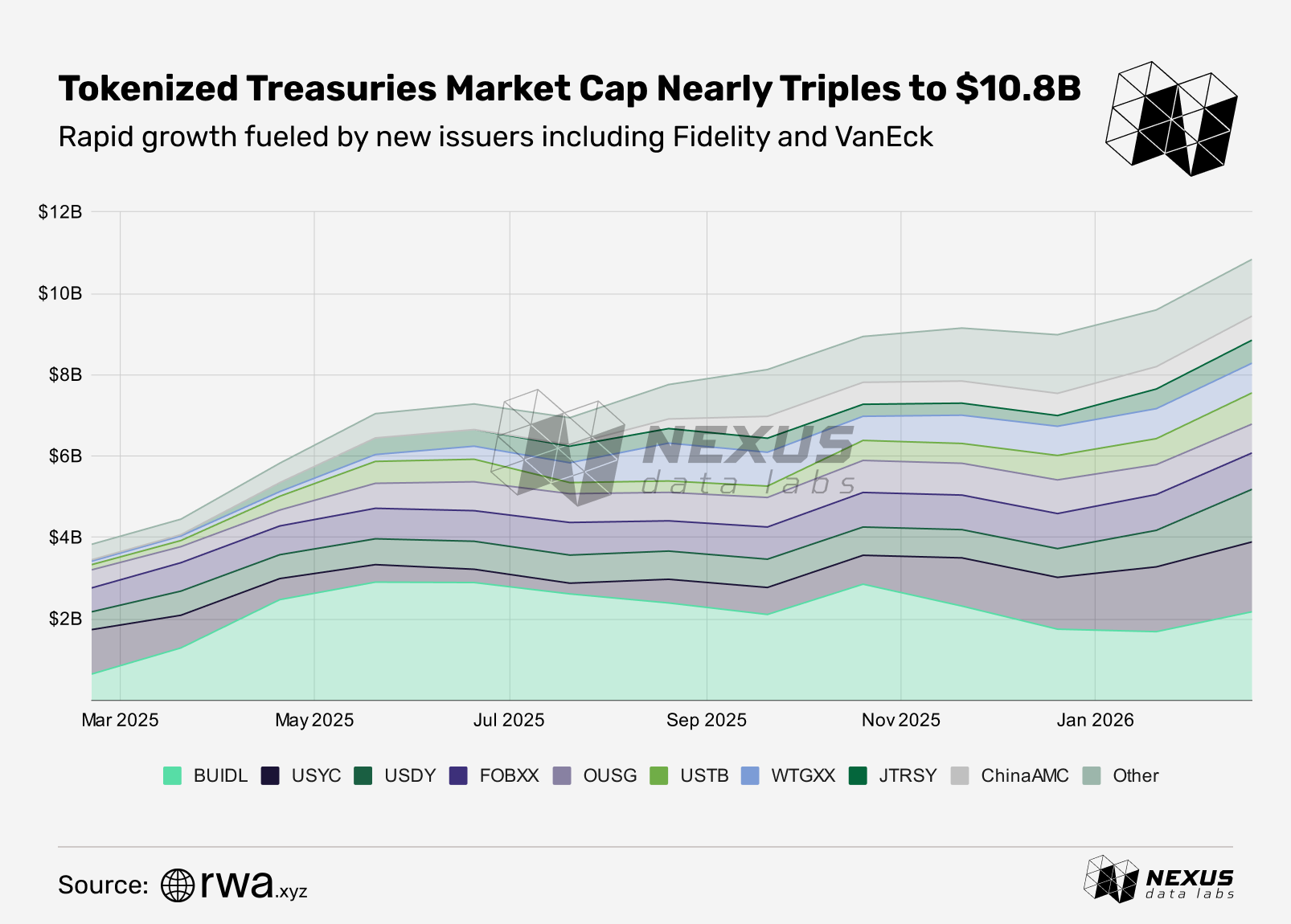

Tokenized U.S. Treasuries reach $10.8B, up 183% year-over-year, as offerings grow from 35 to 53 and top-3 concentration falls from 61% to 48%

Tokenized U.S. Treasuries nearly tripled to $10.8B from $3.8B a year ago (+$7.0B, +183%), with active products growing from 35 to 53 as new funds from Fidelity, ChinaAMC, and VanEck entered the market.

BlackRock's BUIDL rose from $0.6B to $2.2B (+239%), overtaking Hashnote's USYC to become the largest tokenized Treasury product at 20% market share. Ondo's combined exposure — OUSG ($0.7B) and USDY ($1.3B) — reached $2.0B, while newer entrants scaled rapidly: Superstate's USTB ($0.8B, +499%), WisdomTree's WTGXX ($0.7B, +759%), and ChinaAMC ($0.6B, from $0). Together, these dynamics pushed top-3 concentration down from 61% to 48%, reflecting a more fragmented and competitive market.

Tokenized Stocks

Frederick Hopkins | Website | Dashboard

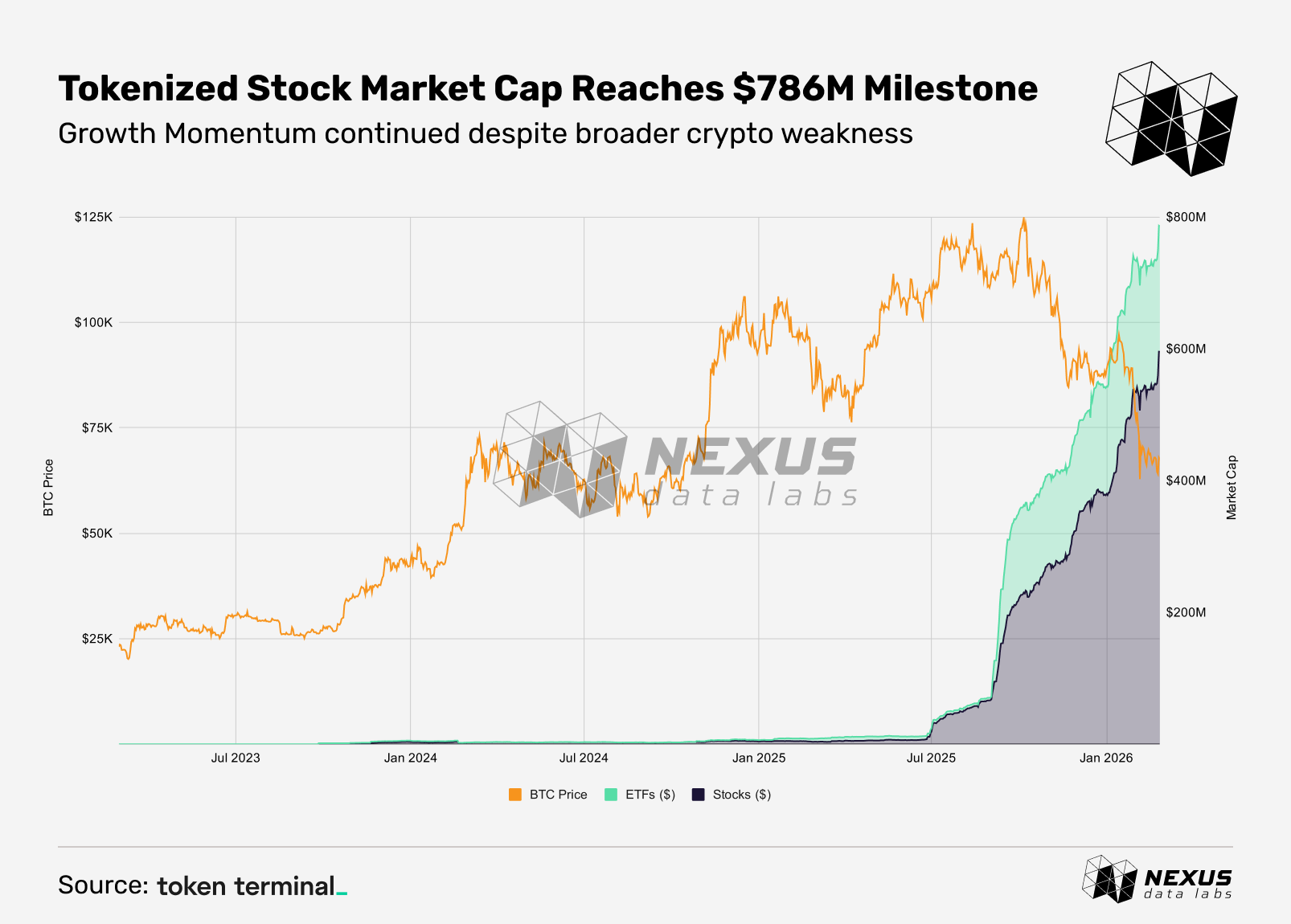

Tokenized stocks grew from near-zero to $786M since mid-2025, making them the newest yet fastest-growing category of tokenized assets

Since mid-2025, tokenized stocks have scaled from near-zero to $786M — driven by a expanding roster of issuers including Ondo Finance, Backed Finance, Spiko, Robinhood, Dinari, Remora Markets, and Superstate. These platforms tokenize both individual equities — NVDA, GOOGL, and TSLA — and ETFs like SPY and QQQ, which track the S&P 500 and Nasdaq-100, enabling 24/7 trading with near-instant settlement.

Market cap growth accelerated even as Bitcoin dropped below $70K — a sign that onchain demand for equity exposure may be developing independently of broader crypto market sentiment.

Tokenized Gold

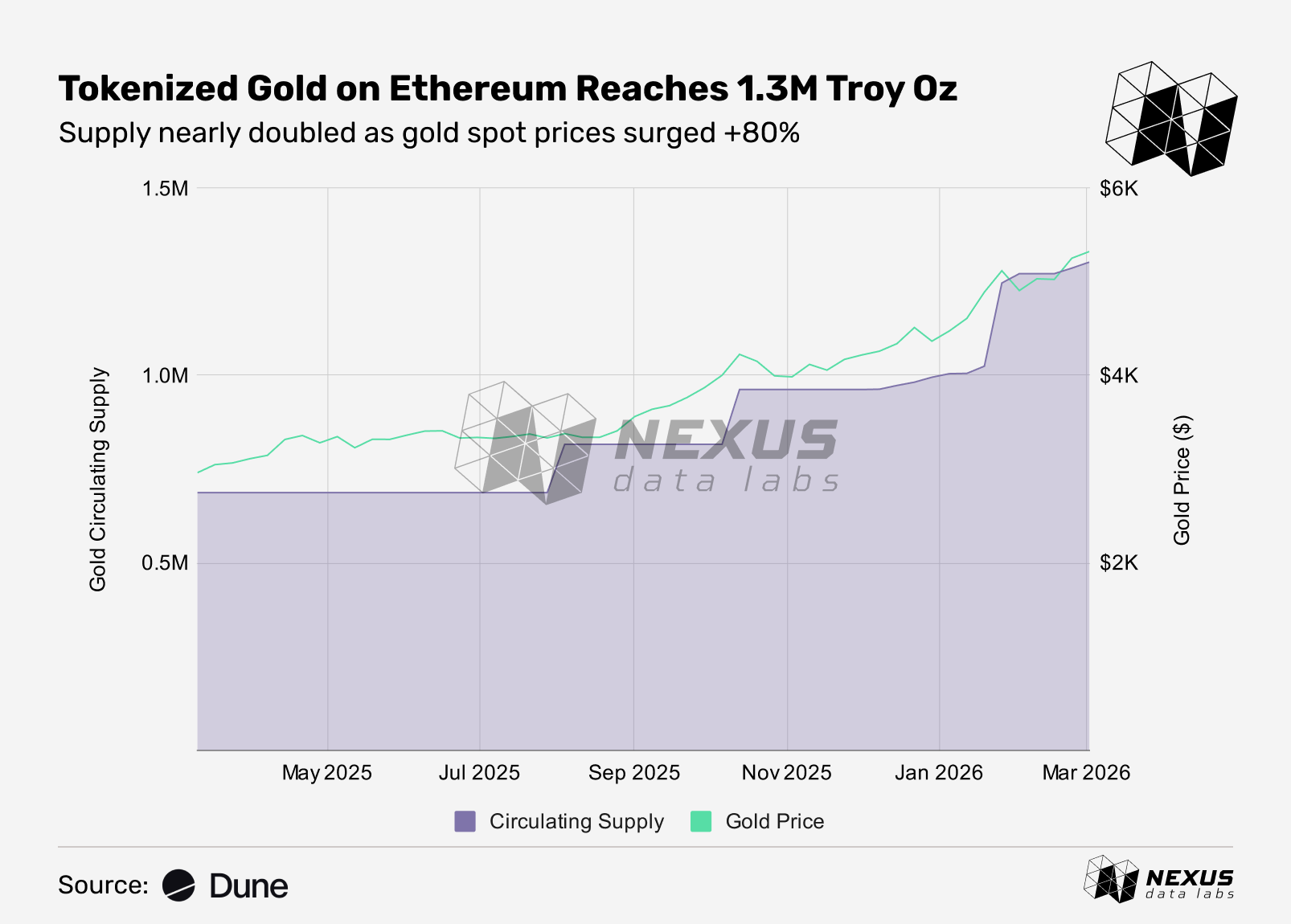

Tokenized gold circulating supply nearly doubled from 687K to 1.3M troy oz over the past 12 months, as gold spot price surged 80% from $2,963 to $5,327

Onchain tokenized gold (PAXG, XAUT, CACHE, AWG, PMGT on Ethereum) grew its combined circulating supply from ~687K troy oz in March 2025 to over 1.3M troy oz by March 2026, a ~90% increase over 12 months. Over the same period, the gold spot price rose from $2,963 to $5,327 (+80%), with a clear supply acceleration starting in August 2025 as gold broke new highs.

Notably, supply growth outpaced price appreciation, suggesting investors were actively minting new tokenized gold rather than simply riding the price rally. Tokenized gold appears to be evolving from a niche wrapper into a blockchain-integrated store of value and macro hedge.

RWA Use in DeFi

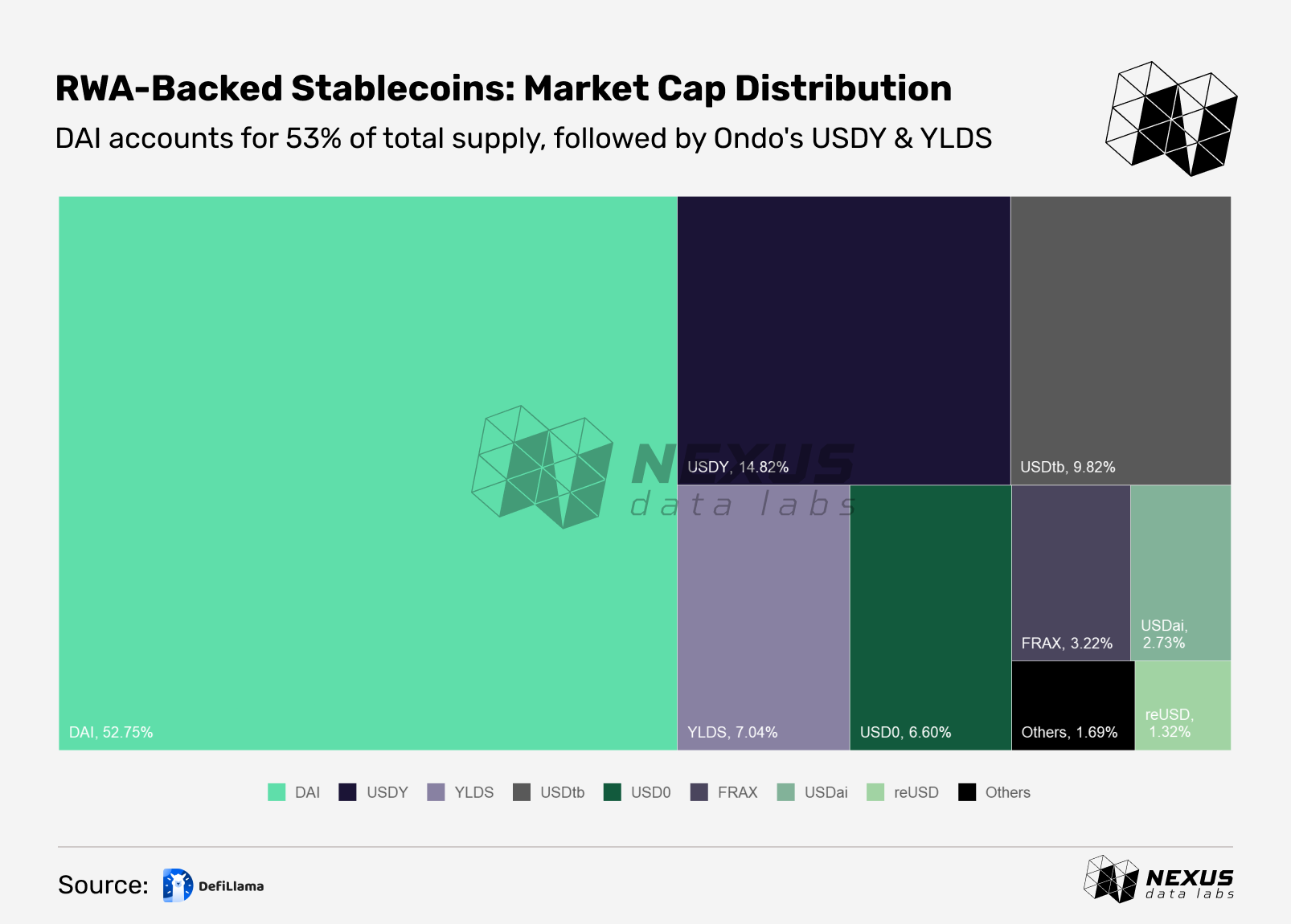

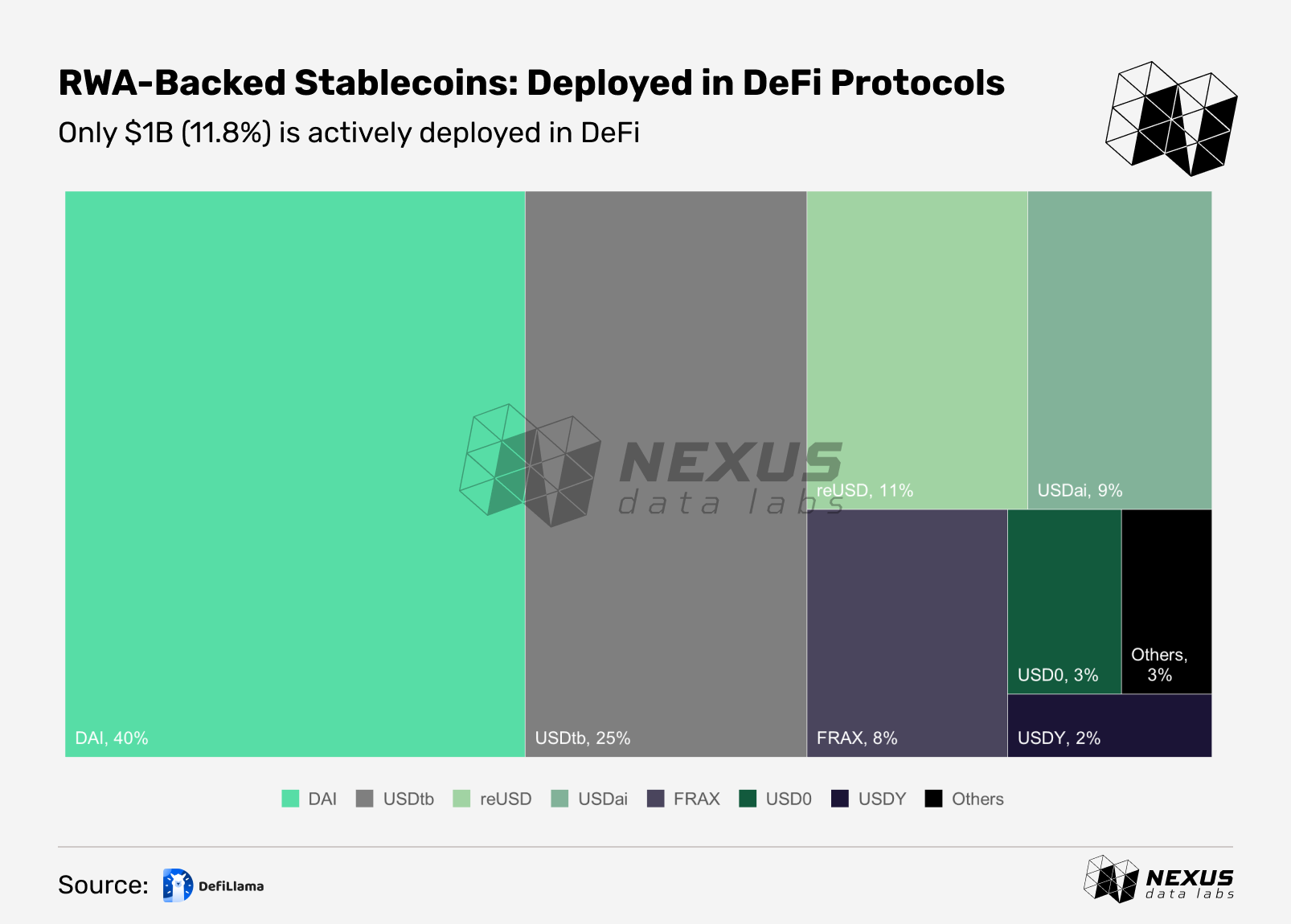

Only 11.8% of RWA-Backed Stablecoins are Actually Used in DeFi

According to DeFiLlama, there is $8.49B in active RWA-backed stablecoin supply, but only $1B (11.8%) is deployed across DeFi protocols.

By RWA-backed stablecoin market cap, DAI dominates with 53% ($4.48B), followed by Ondo’s USDY (15%, $1.26B) and YLDS (7%, $598M). Yet when filtering for RWA-backed stablecoins actively used in DeFi, the picture flips. USDY collapses to just 1.99% of RWA-backed stablecoin usage in DeFi and YLDS vanishes entirely. Meanwhile, USDtb and reUSD surge to 24.6% and 10.85%, respectively.

The reason is straightforward: access restrictions. Permissioned tokens that require KYC, whitelisting, or holder limitations cannot integrate seamlessly with permissionless DeFi contracts, so their onchain utilization can drop to zero. As a result, USDY and YLDS, worth a combined $1.86B, virtually disappear from the active DeFi TVL view. In contrast, permissionless assets show meaningful DeFi utilization: 96.7% of reUSD, 39.1% of USDai, 29.5% of USDtb, and 28.0% of legacy FRAX.

Zooming out, the picture is clear: $7.49B, roughly 88% of RWA-backed stablecoin supply, remains outside DeFi. Composability is limited when access restrictions meet permissionless infrastructure.

Closing Thoughts

Institutional capital is putting assets onchain, and DeFi protocols are developing ways to put those assets to work, but the real challenge lies in creating true capital efficiency once those assets land onchain.

Without active integration with DeFi, RWAs risk becoming little more than mirrored ledgers; transparent, but idle. The next phase of growth will hinge on designing mechanisms that connect these tokenized assets to onchain liquidity, credit, and governance layers.

Further, as RWA markets mature, so must the frameworks used to analyze them. Traditional asset labels, while widely used, can be incomplete. Once tokenized, these assets carry two additional layers of risk beyond simple exposure: the risk of the digital asset issuer, and the risk of the blockchain infrastructure. Ignoring these layers can lead to an incomplete assessment of a tokenized asset’s true risk profile.

What We're Watching

Next Week

For Nexus’ next issue, we turn to Perpetual DEXs, exploring how decentralized derivatives infrastructure is maturing and what that means for onchain market structure.