Nexus Data #007 - Non-USD Stablecoins

Welcome to the seventh edition of Nexus Data Labs, where we highlight what matters most in the fast-developing world of onchain finance.

Thank you to Filippo, J.W., Owen, and Diego for contributing to this issue.

What We're Building

Over the past few weeks, Nexus has been working with Token Terminal to build a local stablecoins dashboard. That work became the spark for this issue. The further we went into the data, the clearer it became that non-USD stablecoins deserve dedicated analysis. The dashboard is still a work in progress, and we welcome feedback as we continue to refine it.

Setting the Scene

Stablecoins have found one of the clearest product-market fits in crypto. Total supply has crossed $294B, with USDT and USDC accounting for ~85% of the market. But that dominance obscures a structural gap.

In global FX markets, the US dollar is involved in 89% of transactions. Every one of those trades has a second currency on the other side. Onchain, that second half barely exists. Non-USD stablecoins represent just 0.33% of total stablecoin supply. The global economy is multi-currency, but onchain finance is not.

That gap is a product of how the market was built. Early stablecoins were designed for traders, and dollar-denominated liquidity became the default unit of account, collateral, and settlement layer across crypto. That works for a fraction of the world. For most of the world, transacting in USD stablecoins introduces constant FX exposure into everyday financial activity. Local stablecoins flip that equation. The rails stay global, but the unit of account becomes local.

This week, we cover the leading stablecoins across three non-USD currency segments: $EURC for euros, $ZCHF for the Swiss franc, and $BRZ for the Brazilian real.

Overview

Non-USD stablecoin supply crosses $2.3B, but growth and adoption tell different stories

According to Dune, non-USD stablecoin supply has crossed $2.3B, expanding 2.3x in 12 months. But the distribution behind that number is uneven, and the headline figure obscures a fragmented picture beneath it.

A7A5, a ruble-pegged stablecoin, accounts for the largest share of that growth, expanding 8.4x to $1.17B across 36K wallets. EURC reached $476M, up 1.8x, with 203K holders and the widest retail distribution among large non-USD stablecoins. JPYC went from a single holder to 45K in under a year, the fastest onboarding ramp in the category. EURA still reports roughly 797K holders against only $4M in supply, and with Angle Protocol announcing its discontinuation in March 2026, that holder base is winding down.

Euro-pegged stablecoins remain the most diverse category by both supply and holder count. But across the broader non-USD landscape, supply growth and holder growth are moving at different speeds and in different directions.

Euro Stablecoins ($EURC)

Owen Fernau | Website | Dashboard

EURC holder count grows 2.2x faster than supply

EURC, a euro-pegged stablecoin issued by Circle, is the largest non-USD stablecoin by market cap at $476M, representing just over half of all non-USD stablecoin supply combined. This excludes A7A5, a ruble-pegged stablecoin that, due to international sanctions on Russia, is not tracked by most data providers.

Since January 2025, supply has grown 286% while holder count climbed 633%, with holders growing 2.2x faster than supply. One interpretation is that EURC is becoming diluted as new holders enter. Each holder represents a proportionally smaller share of total supply than 16 months ago, even as overall supply has expanded. That pattern is consistent with organic adoption rather than concentration.

EURC's growth story points toward broader distribution. The question now is whether Circle can convert that expanding base into an actively transacting network, or whether EURC settles into a compliance-driven store of value rather than a functioning payments rail.

Frankencoin ($ZCHF)

ZCHF market cap reaches $38M with 89% growth in 2026

Frankencoin (ZCHF) is the largest CHF stablecoin onchain, pegged 1:1 to the Swiss franc. Unlike USDT or USDC, no company holds reserves in a bank account to back it. ZCHF is minted by users who lock up crypto as collateral directly onchain, and if that collateral loses value, it is liquidated automatically to protect the peg.

The mechanism is deliberately different from most collateralized stablecoins. Rather than relying on external price feeds to trigger liquidations, ZCHF uses an auction process. When a position is challenged, the market bids on the collateral over a period of days rather than minutes. The architecture makes it slower, but removes a vulnerability that has cost DeFi protocols hundreds of millions in oracle manipulation attacks. A set of economic constraints pushes the market toward parity from two sides, incentivizing arbitrage whenever ZCHF deviates.

The protocol runs on two tokens. ZCHF is the stablecoin. Frankencoin Pool Shares (FPS) represent ownership in the protocol. FPS holders earn protocol fees and liquidation proceeds, but they are also the first to absorb losses if the system becomes undercollateralized.

ZCHF's market cap reached $38M while average wallet balance declined from roughly $90K to under $25K. Early data suggests organic adoption may be broadening beyond the protocol's early users, though it is too soon to draw firm conclusions. Average balance alone captures only one dimension of that distribution. Growing market cap paired with an expanding holder base will determine whether ZCHF's trajectory reflects structural demand or remains a niche footnote in the stablecoin market. Until that scale is reached, ZCHF remains a proof of concept rather than a functioning alternative to dollar-based stablecoins.

Brazilian Digital ($BRZ)

Diego Cabral | Website | Dashboard

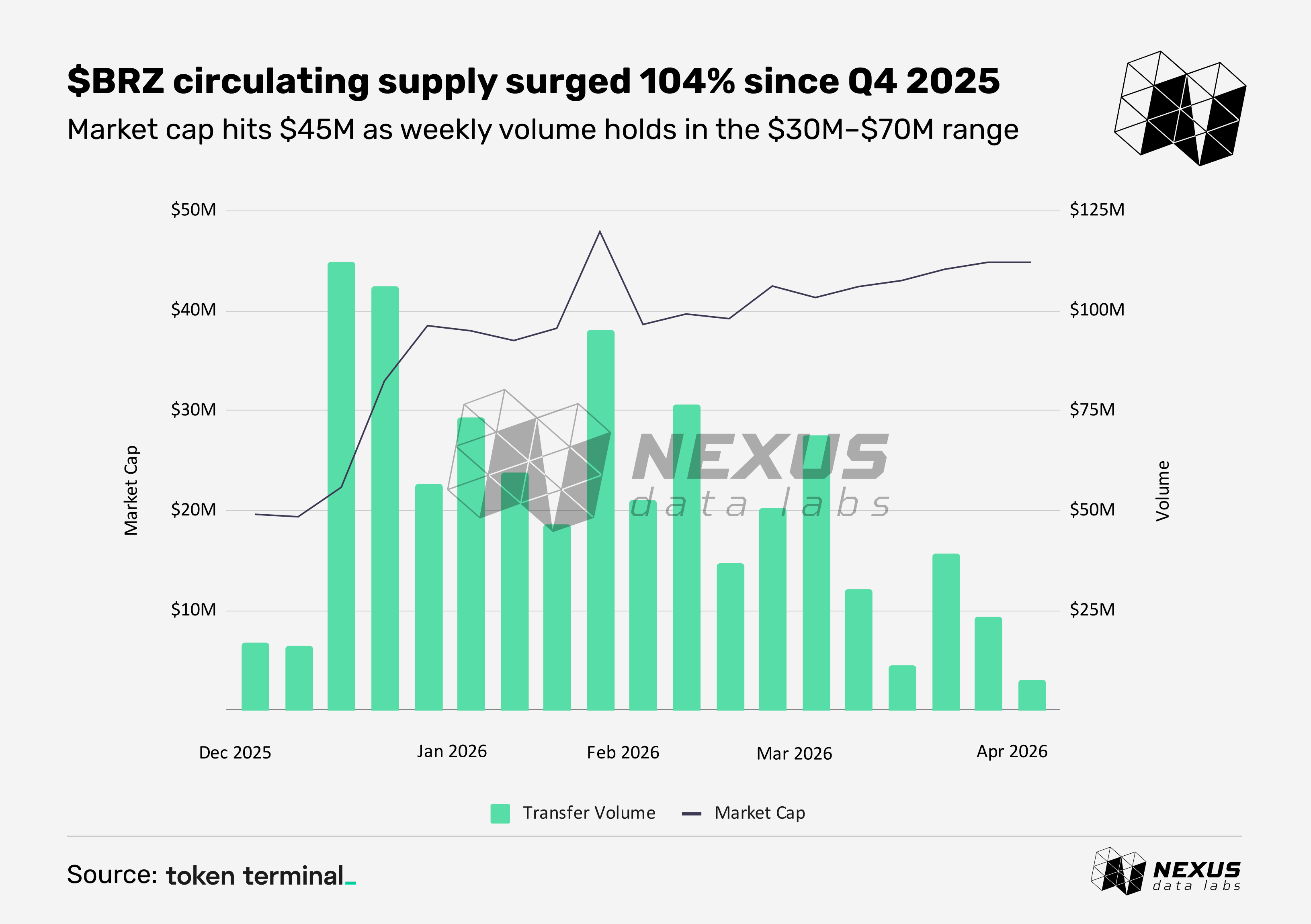

BRZ has processed $980M in volume in 2026 on $44.8M circulating supply

Transfero’s BRZ is the largest BRL-pegged stablecoin onchain, with $44.8M in circulating supply and $980M in transfer volume year to date. That is roughly a 20x supply turnover, a ratio more consistent with an active payment rail than a parked store of value.

Since early December 2025, circulating supply expanded rapidly from $19.7M to $44.8M, a 127% increase in under four months. Weekly transfer volume has held in the $30M to $70M range throughout.

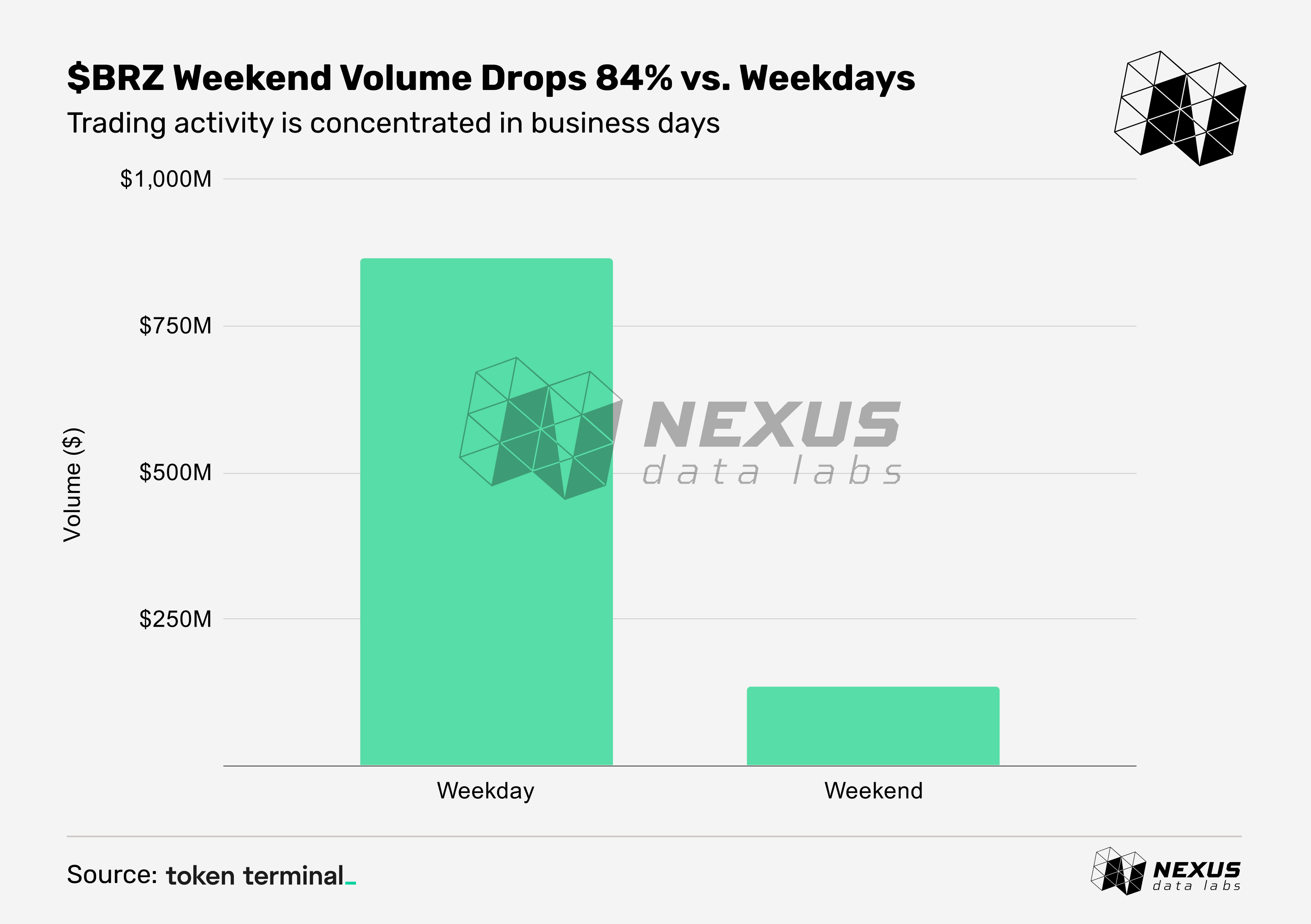

On average, BRZ transfer volume drops 84% on weekends compared to weekdays. The average weekday sits around $14.7M while weekends come in at $3.4M. That pattern is a direct signal of payment orientation, consistent with payroll and B2B settlement cycles rather than speculative trading. Usage is leading supply growth, not the other way around. That is what a local-currency stablecoin functioning as a real payment tool looks like.

Editor's Note

The following two transactions are excluded from this analysis. The mint and burn activity appears to artificially inflate transfer volume:

0xca380e327a8c45c47624f55f8bf1d12c1c1c596ec84199e080d04e910e10b8e0

0x07697bc316c89a8134e98eddf1076a88260e8c02d77e70cbdbdca14f707109e4

Closing Thoughts

The US dollar is the world's reserve currency, and dollar-denominated liquidity was the natural starting point for a market built on global, permissionless rails. Dollar stablecoins won because they arrived first and solved the right problem for the right users at the right time. That progression made sense.

Local stablecoins represent the next phase. Not as competitors to USDT or USDC, but as missing infrastructure. As adoption moves from trading to payments, payroll, and treasury flows, the demand for onchain money that matches real-world liabilities becomes unavoidable. A business paying suppliers in euros, a freelancer receiving income in Japanese yen, a Swiss firm settling invoices in francs. None of them are naturally dollar users. Onchain rails that ignore that reality will remain incomplete.

What EURC, ZCHF, and BRZ each show, at different stages of maturity, is that local demand exists and is measurable onchain. The growth is uneven and liquidity remains thin relative to USD pairs, but the foundation is being laid. The next stage of stablecoin growth will not be won by one currency. It will be built currency by currency.

What We’re Watching

Web3 Data Jobs

Nexus is partnering with Unchain Data to highlight opportunities across the onchain data ecosystem. This week’s featured openings: