Nexus Data #015 - RWA

Where Wall Street's Assets Go Onchain

Intro

Welcome to the fifteenth edition of Nexus Data Labs, where we highlight what matters most in the fast-developing world of onchain finance.

Thank you to Diego, Rizwan, Oğuz, and Frederick for their contributions to this issue.

Setting the Scene

Real-world assets have moved past the proof-of-concept phase. In the past few months, tokenized RWAs have picked up real momentum, pulling traditional finance off the sidelines and into direct participation onchain.

Institutions are no longer debating whether assets belong onchain. The focus now is on which assets make sense. Asset managers are actively experimenting with tokenized Treasuries and money market funds, while other issuers are bringing assets like gold and equities onchain. Each new launch builds on the last, improving settlement, navigating regulatory constraints, and testing where durable demand exists.

The headlines reflect that shift. BlackRock and Franklin Templeton are taking the lead in tokenized Treasuries, while Ondo continues expanding access to onchain yield products. At the same time, more issuers are entering their space, competing for a capital base that was once concentrated in a few permissioned funds. The same firms that defined traditional capital markets are beginning to build their onchain counterparts.

This week’s edition highlights three sectors of the RWA landscape currently in focus: tokenized Treasuries, tokenized gold, and tokenized ETFs.

Sector Overview

RWA market cap grew 28% to $25.8B since March 2026 as bonds and money market funds extend their lead

Tokenized real-world assets, excluding stablecoins, have reached $25.8B in market cap, up 28% since March 2026 when Nexus first covered the space. That is $5.6B added in under four months. The biggest shift has been in how capital is allocated. Bonds, money market funds, and institutional debt have climbed 63% to $15.2B, pushing their share of the market from 46% to 59%. At the same time, private credit has declined 10% to $3.0B as yield-focused capital rotates into more liquid fixed-income products.

Precious metals have lost ground, falling 16% to $5.0B, with market share dropping from 30% to 19%. That largely tracks with a pullback in gold prices, reversing the commodity-driven diversification trend seen earlier this year. The fastest-growing segment is tokenized equities, covered last week. Public equities (+129%) and equity indices (+83%) together total a combined market cap of $1.4B, according to DefiLlama, nearly doubling since March 2026 as onchain access to stocks continues to expand. By chain, Ethereum still leads with 58% ($14.6B). BNB Chain has established itself as the clear number two at $3.7B, followed by Stellar ($2.2B) and Solana ($1.8B).

Tokenized Treasury

Tokenized Treasuries cross $15B as BENJI and USDY drive wallet adoption

Tokenized Treasuries have now surpassed $15B in total market cap, but onchain data points to a more nuanced picture than AUM alone suggests. Adoption remains concentrated in a small number of products, led by Ondo’s USDY with $2.1B in supply and Franklin Templeton’s BENJI at $822M. Wallet activity highlights how differently these products are distributed. USDY has 17K total wallets, while BENJI has 1K total wallets.

Institutional-focused products tell a different story. BlackRock’s BUIDL and Hashnote’s USYC hold $2.23B and $3.11B in AUM, respectively, yet BUIDL has just 110 wallets and USYC 47.

Accessibility has been a key driver. Both USDY and BENJI have lowered traditional barriers like $100K minimums and strict whitelisting, opening the door to broader participation and more distributed ownership. Until those constraints ease, capital in tokenized Treasuries is likely to remain concentrated among a small group of participants rather than spreading across a wider base.

Tokenized Gold

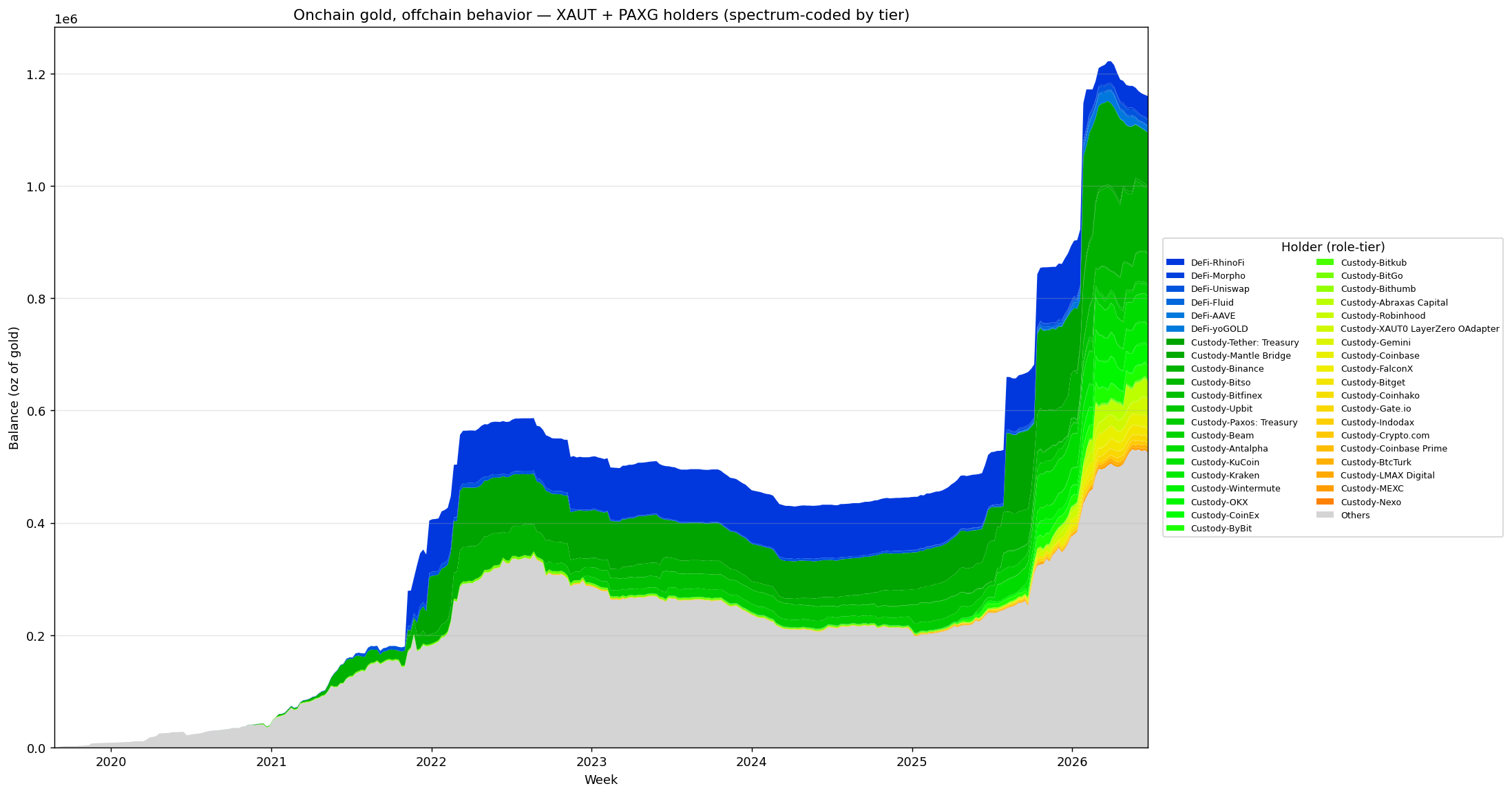

5.6% of tokenized gold sits in DeFi, while 49% sits on CEXs

The total value of tokenized gold peaked at $5.95B in March 2026 and has since declined to $4.5B. The move reflects a pullback in gold prices rather than an exodus from tokenized gold itself. Combined outstanding supply for XAUT and PAXG slipped just 4%, from 1.21M to 1.16M ounces, and these two assets still represent roughly 95% of the market.

An analysis of weekly balances across XAUT and PAXG, with major holders labeled, shows that 49% of supply sits on centralized exchanges (CEXs) and issuer-related wallets, including Tether and Paxos treasuries as well as Binance, Kraken, and Coinbase. In contrast, only 5.6% of supply is deployed across DeFi protocols such as Aave, Morpho, and Uniswap, while the remaining 45% sits in unlabeled addresses.

The data suggests that, despite being onchain, tokenized gold is still used primarily for custody and price exposure rather than active participation in DeFi.

Editor's note: The full breakdown of institutions within each category can be explored in detail here

{kind=link}

Tokenized ETFs

Top 3 tokenized ETFs track the S&P 500 and account for 32% of the market

The three largest tokenized ETFs by market cap track the S&P 500. As of June 2026, the leading products are IVVon ($69.4M), SPYon ($41.6M), SPYx ($39.6M), IBITon ($39.3M), QQQon ($36.7M), and QQQx ($29.7M). The top three S&P 500 trackers, IVVon, SPYon, and SPYx, hold a combined $148.3M, or 32% of the $450M tokenized ETF market.

This mirrors the structure of traditional markets. In traditional finance, the three largest ETFs globally, Vanguard’s VOO, iShares’ IVV, and State Street’s SPY, all track the S&P 500, and together they dominate ETF assets under management. The same benchmark that anchors traditional portfolios is now emerging as the primary exposure onchain.

Closing Thoughts

The RWA sector is consolidating, not diversifying. Bonds and money market funds now account for 59% of the market, as capital concentrates around the assets that scale most easily. Across categories, the tokens gaining traction are those that are liquid, standardized, and familiar to both institutional and retail investors.

This pattern is not a flaw; it is how new markets typically mature. Liquid, recognizable assets are the first to clear regulatory and operational hurdles, which is why tokenized Treasuries and money market funds are leading adoption.

The next phase will depend less on what gets tokenized and more on how these assets are used. Until RWAs move deeper into the DeFi capital stack by serving as collateral and integrating into onchain trading and settlement, the market will continue to mirror traditional structures more than reshape them.

What We're Watching

Indexed Podcast: AI Is Changing How We Work with Crypto Data

Getting Started with Tokenized Assets: A Guide for Institutional Investors

Web3 Data Jobs

Nexus is partnering with Unchain Data to highlight opportunities across the onchain data ecosystem. This week’s featured openings: