Nexus Opinion - Polygon Has One Anchor Tenant: Polymarket

By J.W.

The article is also available on X

Setting the Scene

Polygon has evolved through several distinct strategic phases since its launch. What began as a scaling solution for Ethereum evolved into a gaming and NFT hub, then a DeFi settlement layer, and most recently a stablecoin and payment network. Across each phase, the underlying message has remained consistent: Polygon is built for broad, real-world adoption at scale.

The data, however, tells a different story.

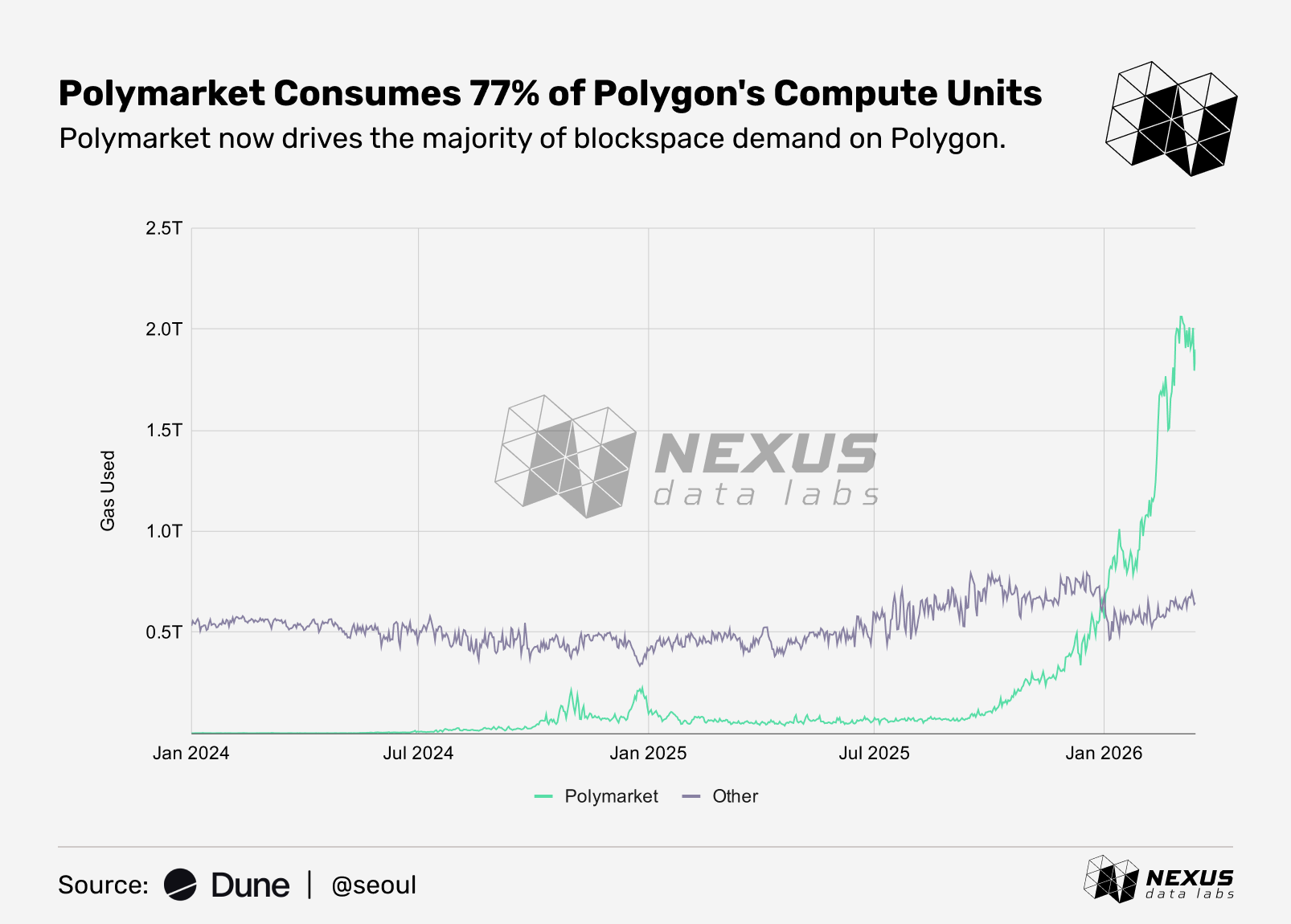

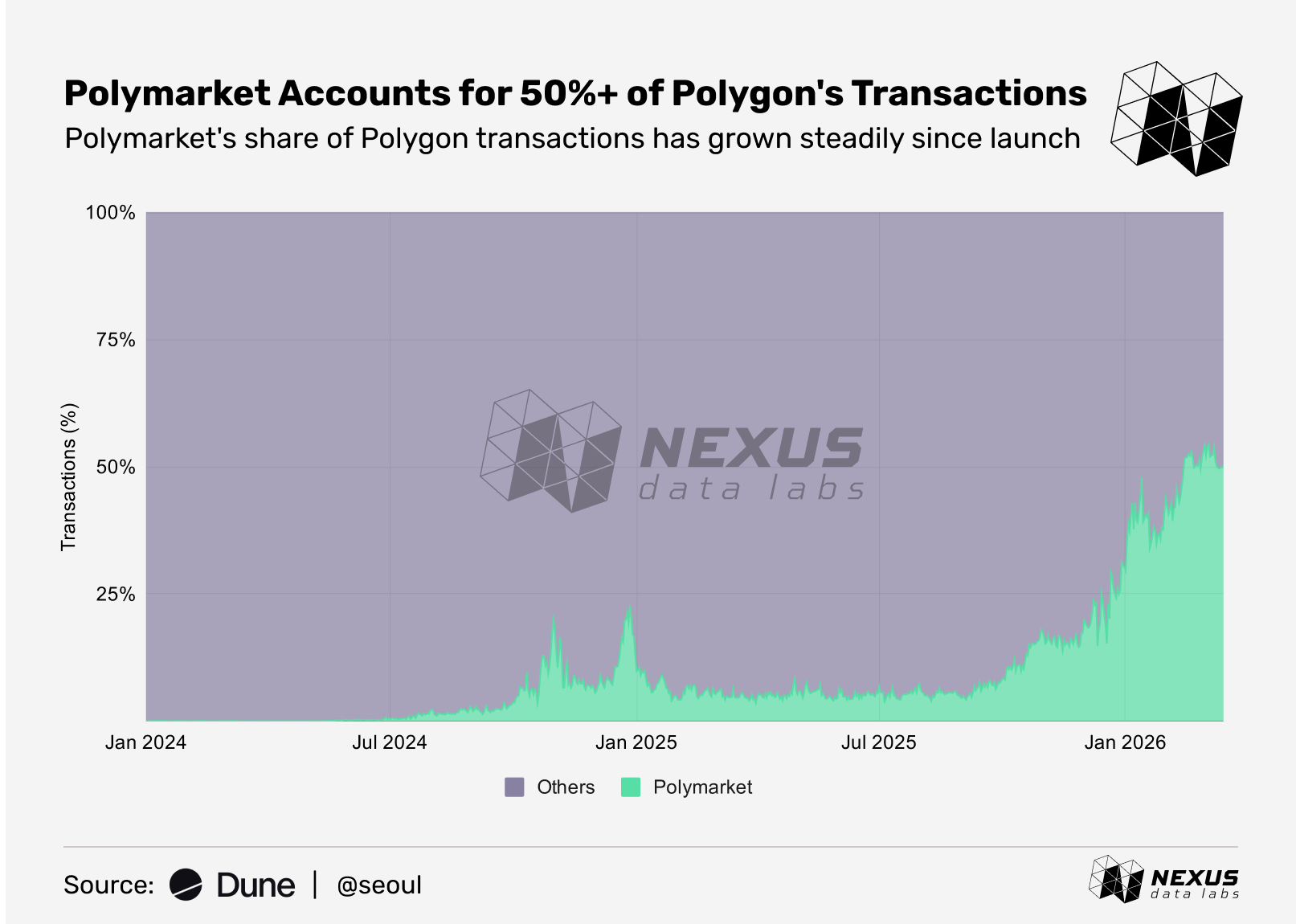

In March 2026, a single application dominated Polygon’s network activity across various measurable dimensions, including transactions and gas fees, according to the Dune Dashboard. That application isn’t a stablecoin issuer or a payment provider. It’s Polymarket. By any infrastructure measure, Polygon’s blockspace economy is not a diverse ecosystem. It is, functionally, a prediction market chain with residual activity surrounding it.

The chain’s stablecoin data reinforces that point. According to RWA.xyz, Polygon hosts approximately $3.6B in stablecoins, a figure central to its payment settlement narrative. However, roughly $1.26B, nearly one in every three dollars, sits inside Polymarket alone: $413M in open interest across markets and $845M in user proxy wallets, according to @datadashboards on Dune. At a time when stablecoin infrastructure is one of the most closely watched growth vectors in crypto, a substantial portion of Polygon’s stablecoin supply belongs to a prediction market, not a payment protocol.

The Bear Case: Polygon's Single-App Problem

Polygon markets itself as "the go-to blockchain for global payments," positioning its chain as infrastructure for payments and stablecoins. In traditional financial infrastructure, settlement layers derive their resilience from diversity of demand. The more independent sources of fee revenue a settlement layer has, the more resilient its economic foundation becomes. This is not a crypto-native concept. It is the same logic that underpins payment rails and correspondent banking networks.

By that standard, the data presents a challenge for Polygon’s current positioning. A network where one application accounts for the majority of gas fees and compute load does not reflect the profile of a settlement layer. As of March 2026, Polymarket’s share of Polygon’s network activity tells that story plainly:

Gas fees: 67.3%

Compute units: 77.0%

Transactions: 54.4%

It reflects a network where one protocol drives the majority of demand and everything else is residual. That concentration creates a structural dependency. Polygon’s fee revenue, throughput economics, and network utilization are substantially driven by a single protocol’s activity. At this scale, that concentration could pose a systemic risk to the network itself.

The Dependency Risk: What Happens If Polymarket Leaves?

This is not a hypothetical. Application-specific chains have become a trend with dYdX and Uniswap launching their own execution environments rather than remaining deployed as apps on shared networks. Polymarket has equal incentive to pursue its own chain as well. As the platform scales, the case for Polymarket controlling its own execution environment strengthens. A Polymarket L2 would preserve settlement flexibility while capturing fee revenue that currently accrues to Polygon validators.

If Polymarket migrates, Polygon does not gradually lose activity. It loses it overnight. Fee revenue collapses. Transaction volume craters. There is no second application waiting to absorb the load, at least not yet. What remains is a chain that once hosted the world's largest prediction market, now competing for relevance with a significantly thinner demand base, unless another Polymarket comes along.

The Bull Case: Polygon’s Memecoin Moment

Despite the bear case built around Polymarket’s concentration, there is a credible counterargument. Polygon’s relationship with Polymarket mirrors Solana’s rise in 2024. As memecoin trading volumes exploded, a single sector dominated blockspace demand and fee generation, ultimately driving $SOL’s price appreciation alongside it. So far, however, $POL has not reflected that dynamic in its price performance, despite the structural parallels.

There may be another catalyst on the horizon. In October 2025, Polymarket CMO Matthew Modabber confirmed that a $POLY token and airdrop are coming, stating “There will be a token, there will be an airdrop.” For Polygon, that confirmation carries implications that extend beyond Polymarket’s own token economy. When $POLY launches, the airdrop creates an entirely new class of economically motivated participants. Recipients will claim tokens, trade them, speculate on price, and rotate into and out of Polymarket to farm further rewards or express views on $POLY itself. Each of those actions generates a transaction that settles on Polygon. A $POLY launch does not just benefit Polymarket in isolation. It would hand Polygon a demand spike, layering a second catalyst on top of a network already running at concentrated capacity. Fee revenue climbs, compute utilization rises, and the network metrics that currently reflect one dominant application compound further, assuming Polymarket stays.

Closing Thoughts

Whether Polymarket ultimately migrates or Polygon captures the $POLY airdrop tailwind remains an open question. Polygon’s relationship with Polymarket is symbiotic, for now. Polymarket gets reliable, low-cost settlement infrastructure. Polygon gets sustained, organic blockspace demand. The arrangement has worked.

In the near term, the arrangement will likely hold. Polymarket’s immediate priority is market share, not chain migration. The fight with Kalshi is accelerating, and building a new execution environment requires resources, engineering time, and operational risk that no platform mid-battle can easily justify. As long as the current infrastructure holds, there is no obvious trigger to move.

But that stability may not last forever. One application controls 77% of Polygon’s compute and holds nearly one in every three dollars of its stablecoin supply. That is a single-app concentration risk embedded in Polygon’s market position, and one the data surfaces whether the narrative acknowledges it or not.