Nexus Opinion - The FX Problem Nobody Has Solved Yet

Sovereign stablecoins are coming. The question is who handles the exchange.

By J.W.

The article is also available on X.

Nexus is building Non-USD Stablecoin Dashboard, powered by Token Terminal, tracking issuance and activity across non-USD denominated stablecoins. The dashboard is a work in progress, and we welcome feedback as we continue to refine it.

The Gap: Non-USD Stablecoins vs. FX Reality

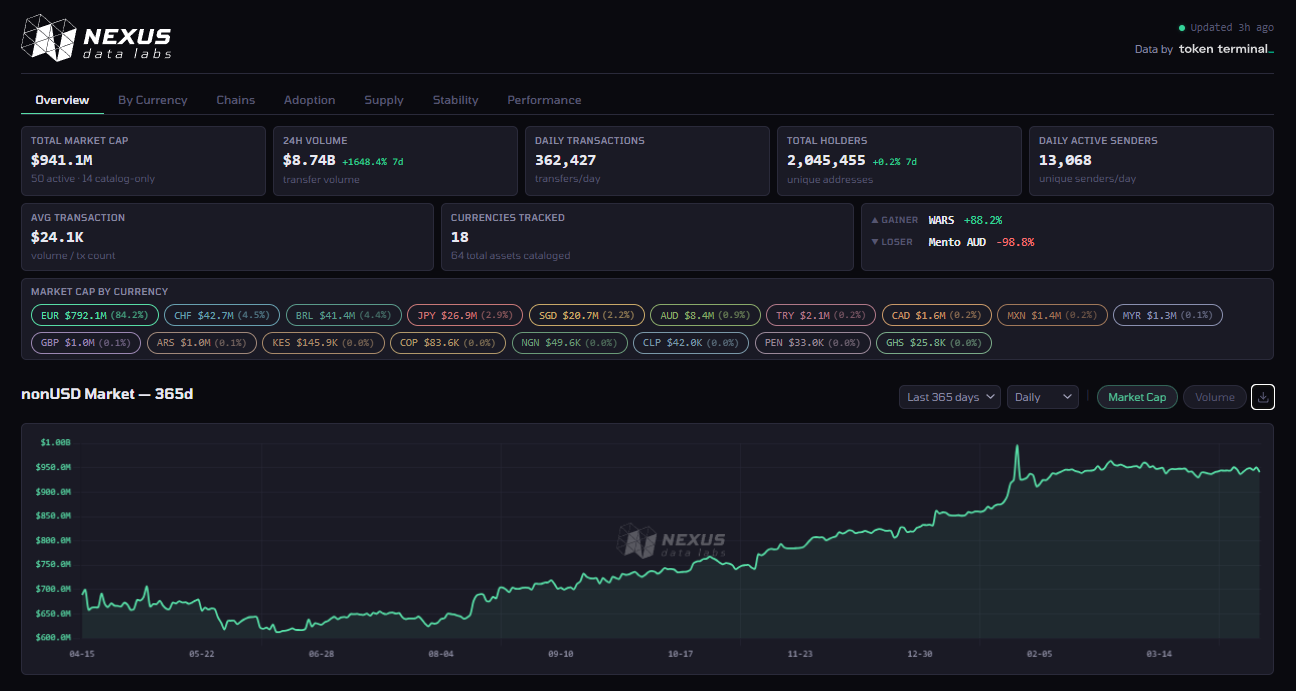

The stablecoin market surpassed $319 billion in April 2026, yet less than 0.3% of that supply is denominated in currencies other than the U.S. dollar. In traditional foreign exchange markets, non-USD currency pairs account for approximately 11% of the roughly $9.6 trillion traded each day. This divergence reflects both market dynamics and an infrastructure gap that has yet to be addressed at scale. The question is whether onchain DEXs, centralized exchanges, or a hybrid architecture of both will emerge as the primary venue for non-USD stablecoin trading.

The momentum behind non-USD stablecoins is clear:

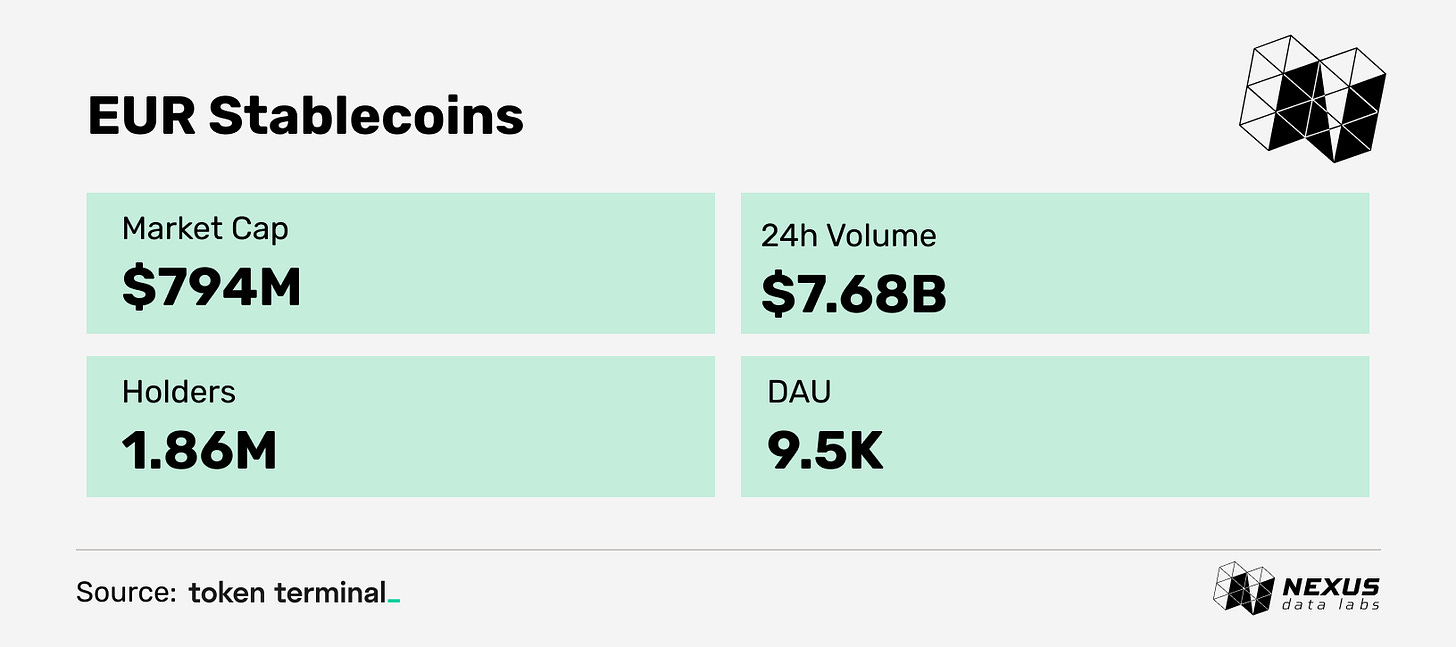

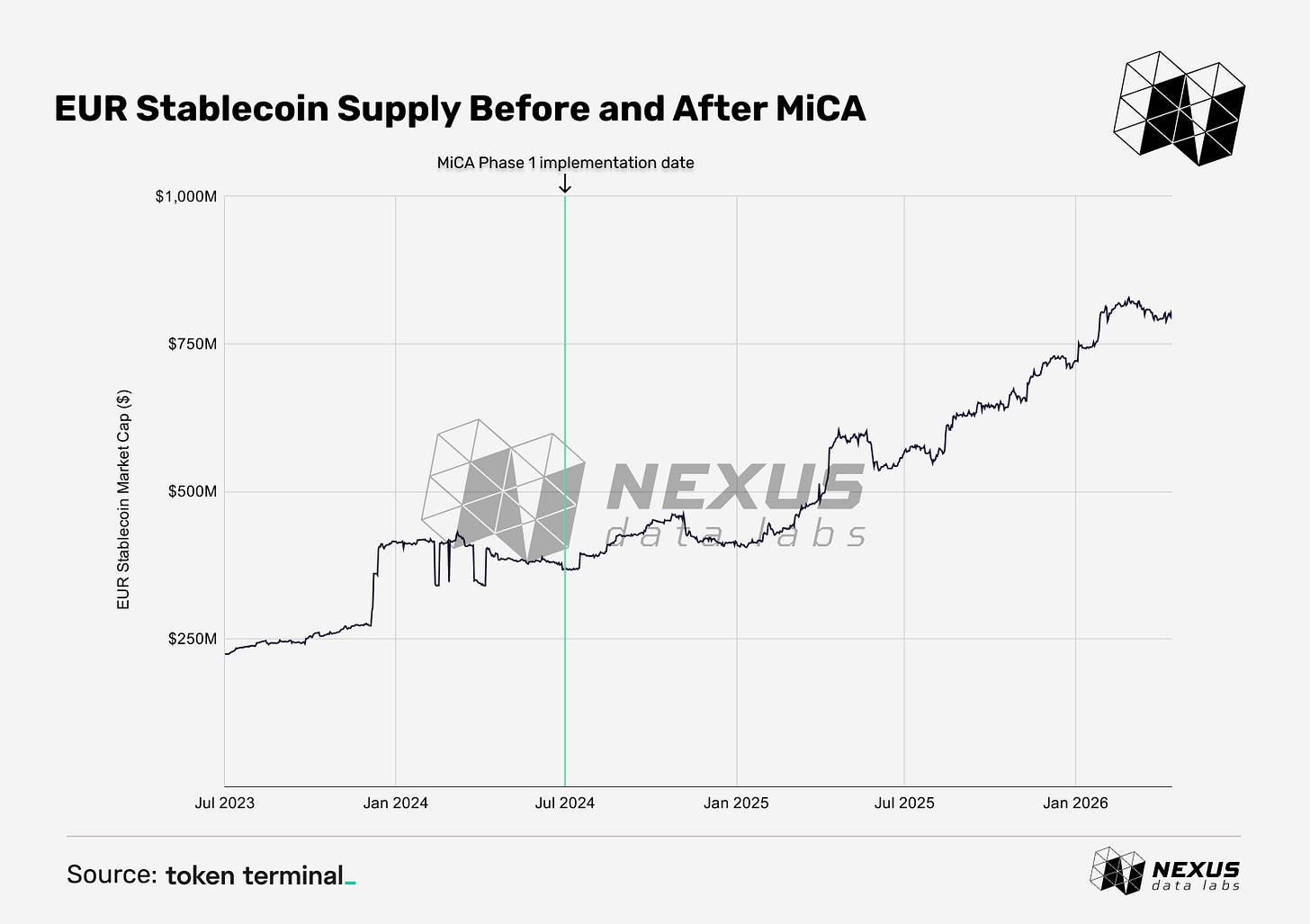

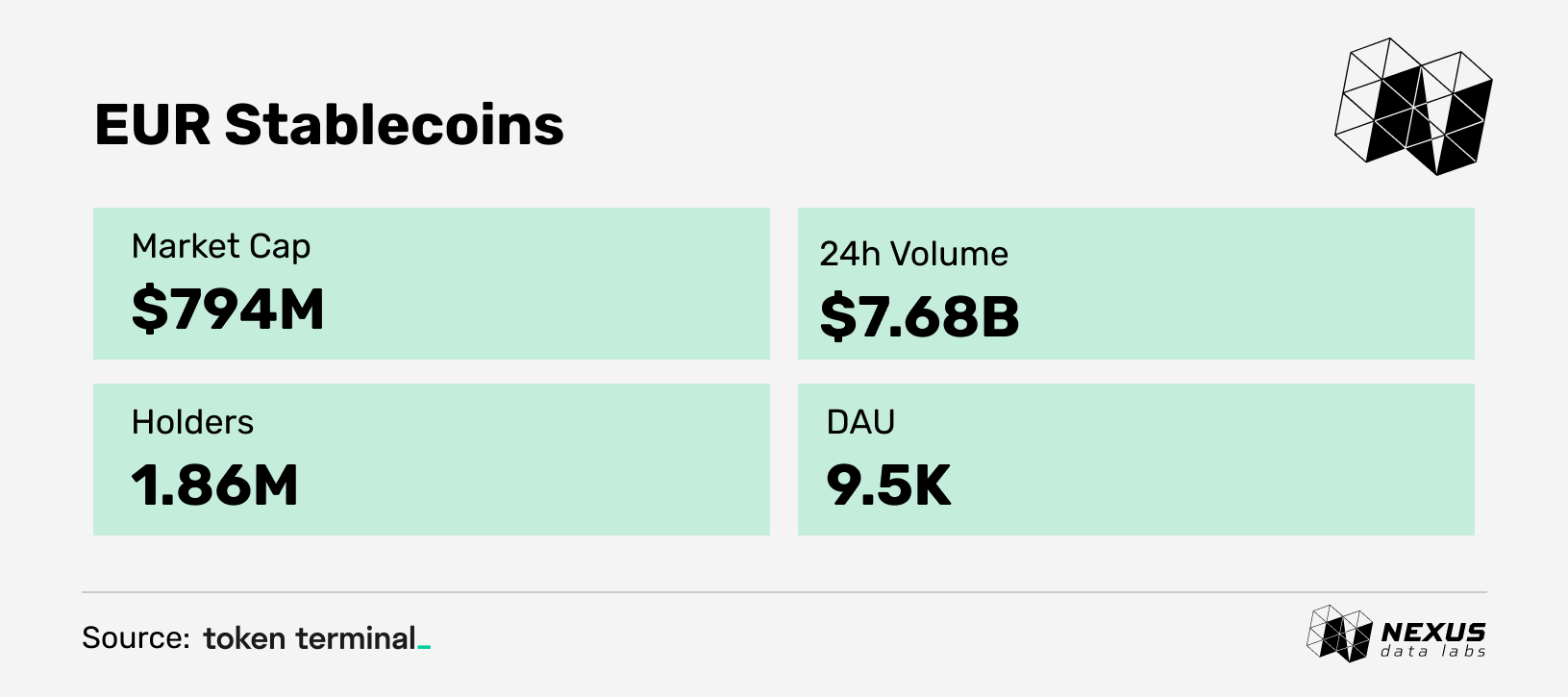

Circle’s EURC became the first MiCA-licensed euro stablecoin in July 2024. Post-MiCA, EURC volumes increased 1,139% and Societe Generale’s EURCV volumes rose 343%. Building on that momentum, a consortium of 12 European banks, including ING, UniCredit, BNP Paribas, and BBVA, formed Qivalis to launch a MiCA-compliant euro stablecoin in H2 2026.

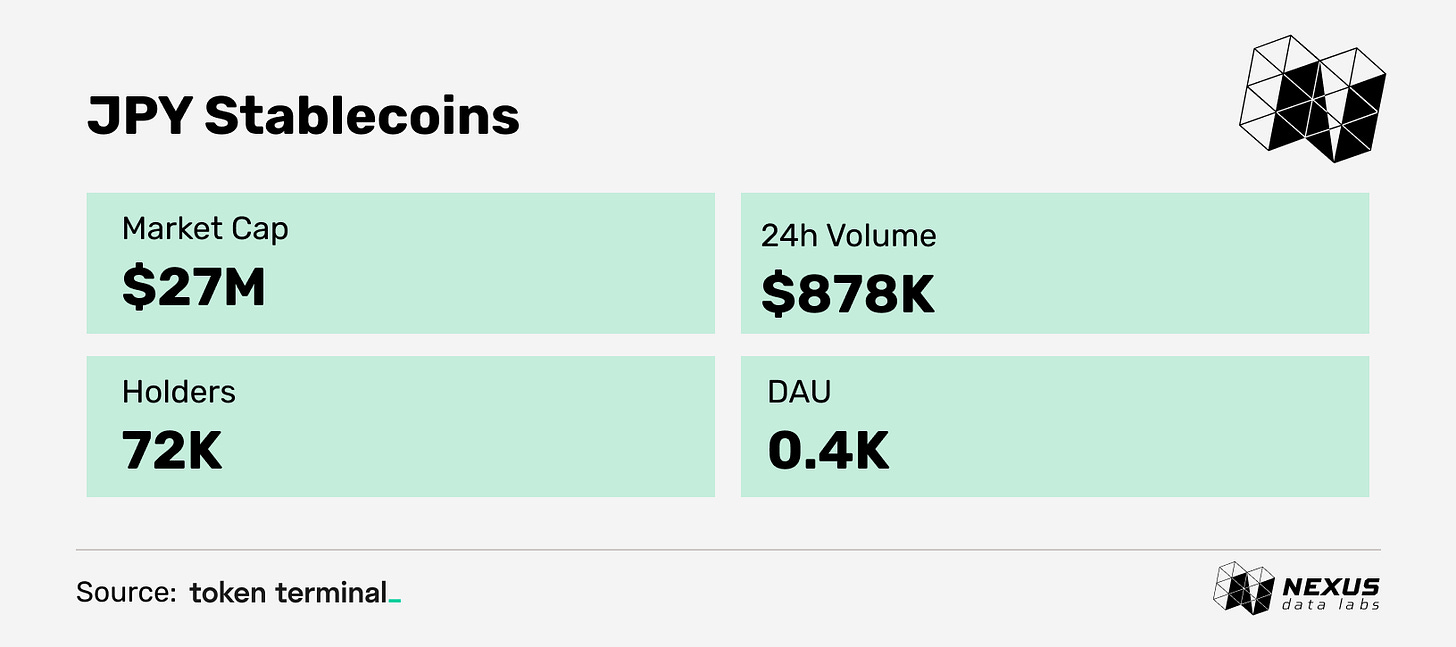

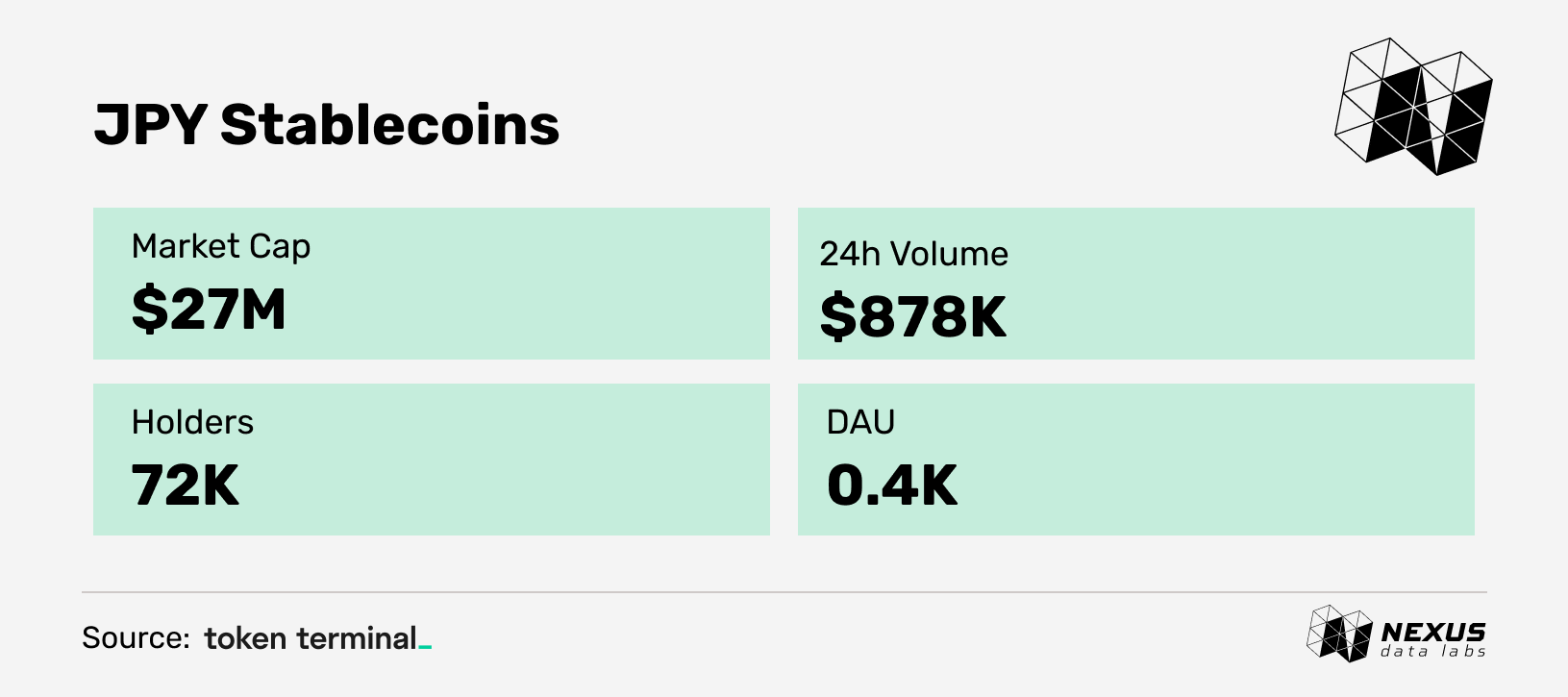

Japan’s JPYC launched as the country’s first regulated yen-backed stablecoin in October 2025, registered under Japan’s Financial Services Agency. Japan’s megabanks (MUFG, SMBC, and Mizuho) launched pilots for stablecoins and tokenized deposits in payments and interbank settlement.

South Korea saw KRW1 launch on Avalanche in September 2025 and KRWQ debut on Coinbase’s Base in October 2025. KakaoBank advanced its won-pegged stablecoin preparations ahead of pending legislation.

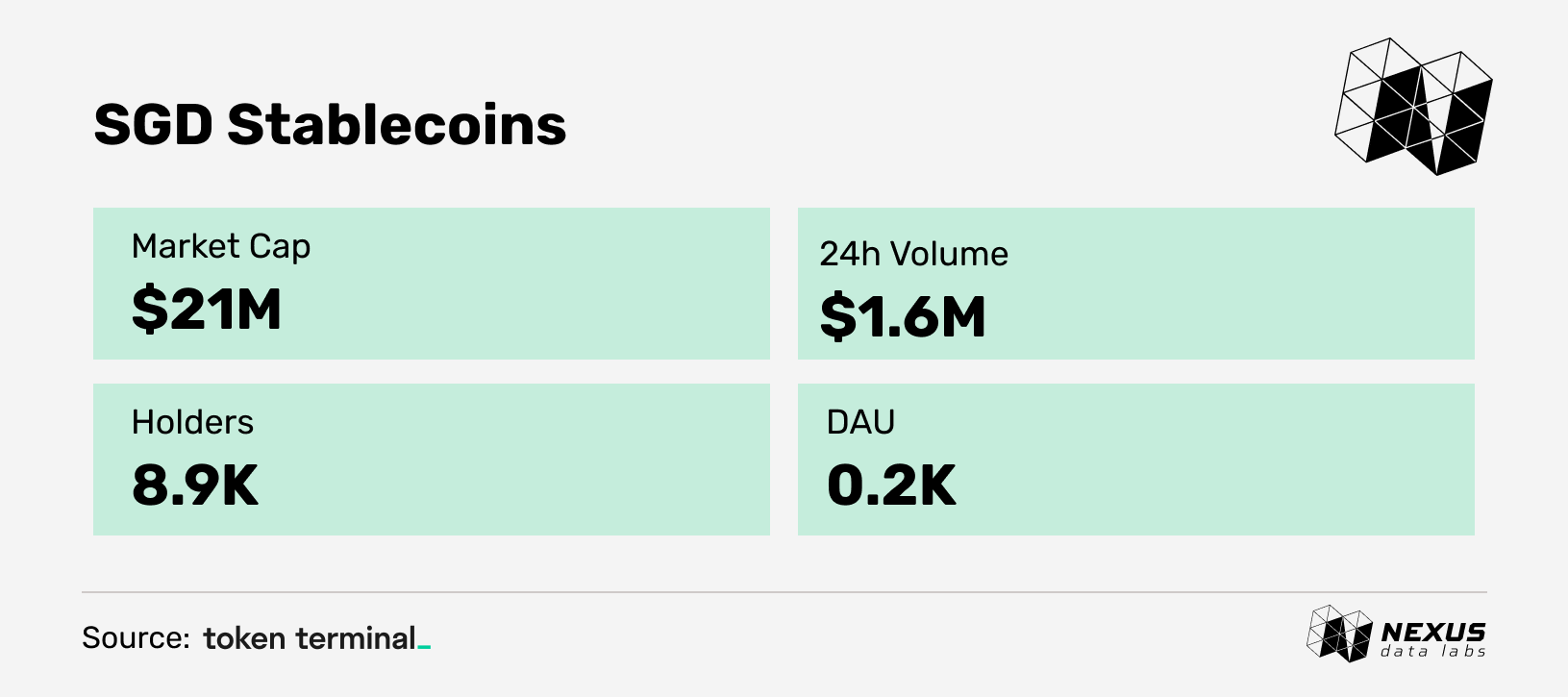

Singapore’s XSGD processed over $3.8B in cumulative onchain volume, expanding into cross-border settlement across ASEAN through partnerships with Grab and Ripple.

The pattern is clear: this is a wave of sovereign stablecoin issuance. Each jurisdiction is effectively betting that its currency deserves a position in the onchain settlement layer. If that bet pays off at scale, one piece of infrastructure becomes essential: the exchange layer between these currencies. The way this layer is designed and governed will determine how deep non-USD liquidity can become, how efficiently flows are routed, and where custodial, credit, and regulatory risks ultimately concentrate.

The FX Architecture Problem

A holder of EURC looking to pay a counterparty in KRW1 faces a structural problem. Today, no direct EURC/KRW1 market offers meaningful liquidity. The practical path requires two legs: EURC to USDC, then USDC to KRW1. Each step incurs costs and routes through the dollar as a pivot currency. This mirrors the pre-digital FX market, where emerging market pairs settled through dollar intermediation and correspondent banks captured spreads at every conversion.

The question is whether onchain infrastructure can compress or eliminate that two-leg structure, and whether DEXs, CEXs, or a hybrid model is best positioned to do so.

The Case for a DEX

Decentralized exchanges enable stablecoin-to-stablecoin swaps without requiring custody, counterparty onboarding, or time zone constraints. Beyond access, composability adds another layer of structural advantage. A DEX-native FX layer can integrate directly with lending protocols, payroll applications, and treasury management tools without bilateral agreements or KYC gatekeeping.

Geographic reach extends that utility further. A DEX deployed on a low-cost L2 can serve a user in Lagos, Bogota, or Manila with identical access and pricing. No correspondent banking relationship required. For emerging markets, this is not a marginal improvement. It is access to a functioning FX market where the local banking system does not provide one.

That model already exists in early form. Mento’s Fixed-Price Market Maker (FPMM) prices swaps against oracle-fed real-world FX reference rates rather than pool dynamics, eliminating the impermanent loss problem that makes traditional AMMs uneconomical for stablecoin LPs. Mento has processed $31B in cumulative DEX volume across 15 currency pairs, according to Artemis.

Where the DEX model breaks down: liquidity. A EURC/KRW1 pool on Uniswap will have far less liquidity than a USDC/KRW1 pool, and far less than either has against the actual Korean won interbank market. Thin liquidity leads to high slippage, and high slippage is a structural tax on every trade. The FPMM oracle approach mitigates pricing instability, but it introduces oracle risk. If the price feed is manipulated or delayed, the pool misprices the swap.

The Case for a CEX / Institutional RFQ Model

Institutional Request for Quote (RFQ) platforms offer a fundamentally different approach to onchain FX. Rather than relying on permissionless liquidity pools, they route price discovery through established market makers and settle onchain, combining the efficiency of traditional FX infrastructure with the speed and finality of blockchain settlement.

The model is already live at institutional scale. Kinexys Digital Payments by JP Morgan enables 24/7 onchain FX settlement across USD, EUR, and GBP for clients including Siemens, Ant International, and B2C2. Circle's StableFX, built on its Arc Layer 1 chain currently in testnet, follows a similar RFQ structure: multiple liquidity providers compete for each trade off-chain, with settlement onchain via smart contract escrow.

Centralized exchanges bring a different but complementary advantage. As more sovereign stablecoins are issued under frameworks like MiCA and the GENIUS Act, Binance, Coinbase, and OKX are well positioned to serve as early liquidity venues for new non-USD pairs, given their existing regulatory relationships and user bases.

The core value of this model is not better pricing. Interbank FX markets are already highly efficient. What the RFQ model offers is faster settlement, reduced counterparty risk, and 24/7 availability. A treasury team managing multicurrency operations does not need tighter spreads. They need to move euros into won at 11pm on a Sunday without waiting for a bank to open.

Where the institutional model breaks down: access. The RFQ model requires bilateral relationships with licensed counterparties. It works for the banks and institutions with Kinexys access. It does nothing for the logistics company in Bangkok that wants to pay a supplier in Mexico City, at least not yet. For businesses and individuals outside institutional onboarding pipelines, that gap is not a minor friction. It is a structural exclusion.

DEX vs. CEX: A Framework

The DEX and CEX models are not competing for the same market. They solve different parts of the FX stack, with structurally distinct addressable markets:

Liquidity depth: CEX dominates major currency pairs. DEX has developed liquidity for established crypto-native pairs but remains structurally thin for emerging market pairs.

Settlement risk: DEX eliminates counterparty exposure. Smart contract escrow ensures both sides settle simultaneously or not at all. CEX achieves equivalent outcomes through RFQ but relies on contractual rather than programmatic guarantees.

Access: DEX is permissionless by design, requiring only a wallet. CEX demands bilateral agreements, KYC onboarding, and licensing, gating institutional quality behind institutional friction.

Composability: DEX can integrate natively with DeFi lending, payroll, and treasury protocols. CEX settlement requires additional steps to deploy in DeFi.

Regulatory posture: CEX operates within familiar banking frameworks. DEX regulatory treatment remains unsettled in most jurisdictions. MiCA’s permissionless DeFi carve-out is provisional.

Geography: DEX is globally accessible and most useful in markets with weak correspondent banking. CEX excels in corridors where both counterparties sit within regulated financial systems.

The most probable outcome is not binary. It is hybrid architecture. Institutional RFQ rails handle wholesale flows between regulated entities. Onchain AMM and FPMM liquidity serves retail, DeFi, and emerging market corridors. The layers are complementary, not competing. The question is which player captures which layer.

Closing Thoughts

Closing the gap between traditional FX markets and non-USD stablecoin pairs will not happen through a single model. In the near term, institutions will gravitate toward centralized venues for the liquidity depth and settlement guarantees they already understand. DEXs are better positioned to start narrow, building liquidity in a few high-volume cross-currency pairs and expanding from there as liquidity deepens and oracle infrastructure matures. The transition will be gradual.

Over time, the DEX model wins on access, composability, and reach, which matters most in emerging markets where correspondent banking is weak and routing through the dollar adds unnecessary friction. The CEX and RFQ model wins on liquidity depth, settlement guarantees, and institutional trust for large wholesale flows. Neither solves the full stack alone. The architecture that ultimately scales will be hybrid.

The most likely path forward mirrors what happened in perpetual DEX markets. Small protocols will launch as experiments, prove product-market fit in specific corridors, and gradually scale into infrastructure. The window to capture that layer is open. But it will not remain so indefinitely.

Sources & Data References

BIS Triennial Central Bank Survey 2025

Token Terminal — Non-USD stablecoin supply, April 2026

Circle — MiCA licensing announcement, July 2024

BBVA — European bank consortium announcement, Feb 2026

Decta — Euro Stablecoin Trends Report 2025

Tiger Research — 2026 Asia Stablecoin Market Overview

The Block — KRW1 on Avalanche, September 2025

The Block — KRWQ on Base, October 2025

CoinDesk — Ripple partnership, May 2025

GeckoTerminal — EURC/USDC pool on Uniswap V3

Artemis — Mento Cumulative DEX volume, April 2026

JP Morgan — Kinexys Digital Payments

Arc Network / Circle — StableFX on Arc testnet, December 2025