Nexus Opinion - The non-USD Stablecoins Landscape

By Diego Cabral

The article is also available on X.

Setting the Scene

One of the fastest-growing sectors of the onchain economy remains largely invisible in mainstream analysis: non-USD stablecoins.

This report breaks down local currency stablecoins, analyzing their metrics, defining how the sector fits into the broader stablecoin landscape, mapping the opportunity, and presenting the data in a way that makes what comes next measurable.

The Problem: Onchain Is a Dollar World. The Real World Isn't.

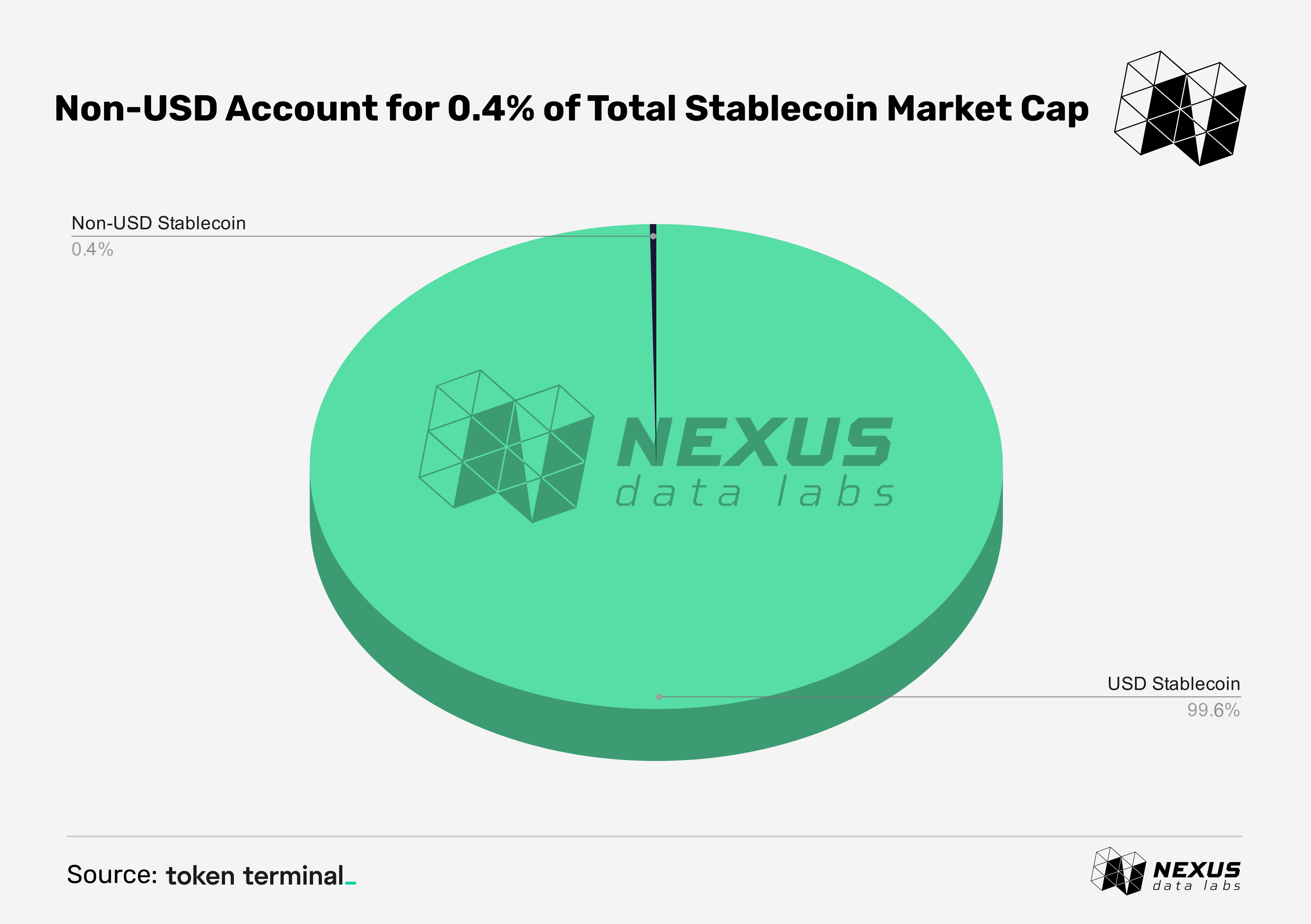

The stablecoin market is one of crypto’s clearest product-market fits, with total supply of $298B. Yet a structural imbalance sits beneath that number. In traditional foreign exchange markets, the US dollar is involved in roughly 89% of all transactions (BIS Triennial Survey, April 2025). In the onchain economy, the concentration is far more extreme: non-USD stablecoins represent just 0.4% of total stablecoin supply.

The gap between how the world transacts and how the onchain economy is structured remains largely unaddressed.

Why Does This Gap Exist?

The stablecoin market was built by and for crypto-native users. Tether launched in 2014 to solve a specific problem: giving traders dollar liquidity without leaving crypto exchanges. That use case defined the entire category, and dollar-pegged stablecoins became the default unit of account, collateral, and settlement across the onchain economy.

For users with stable access to dollar financial services, this works. For the majority of the world, where salaries, taxes, rent, and business expenses are denominated in local currencies, it introduces unwanted FX risk.

Local currency stablecoins move value onchain 24/7, borderless and programmable, while staying denominated in the currency the user actually transacts in.

Non-USD stablecoins are not competing with USDT or USDC. They are completing the onchain economy's infrastructure by serving the part of the global monetary stack that dollar stablecoins, by design, were never built to reach.

Why Now?

There is already clear data showing sustained demand for non-USD stablecoins. Over the past three years, the market cap of local currency stablecoins has grown roughly 3.54x, from $379M to $1.34B.

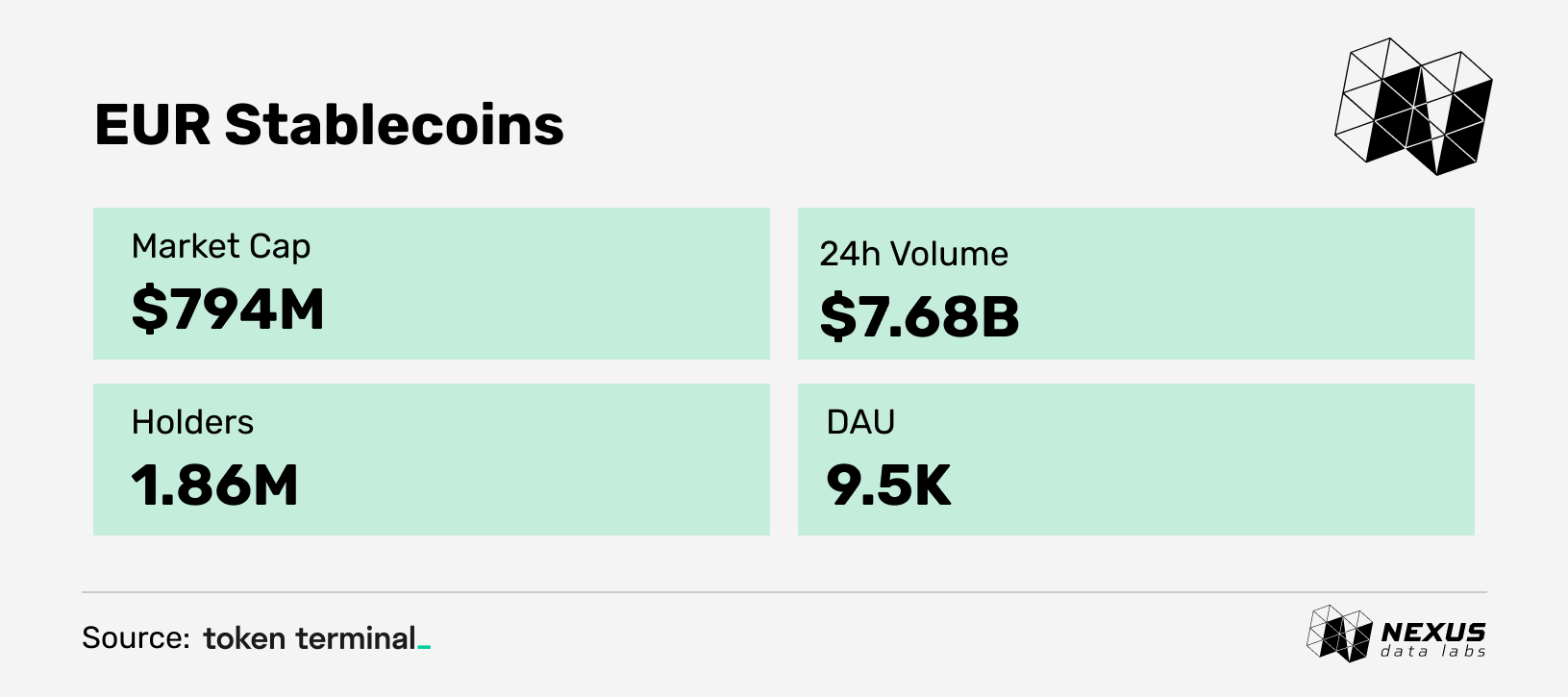

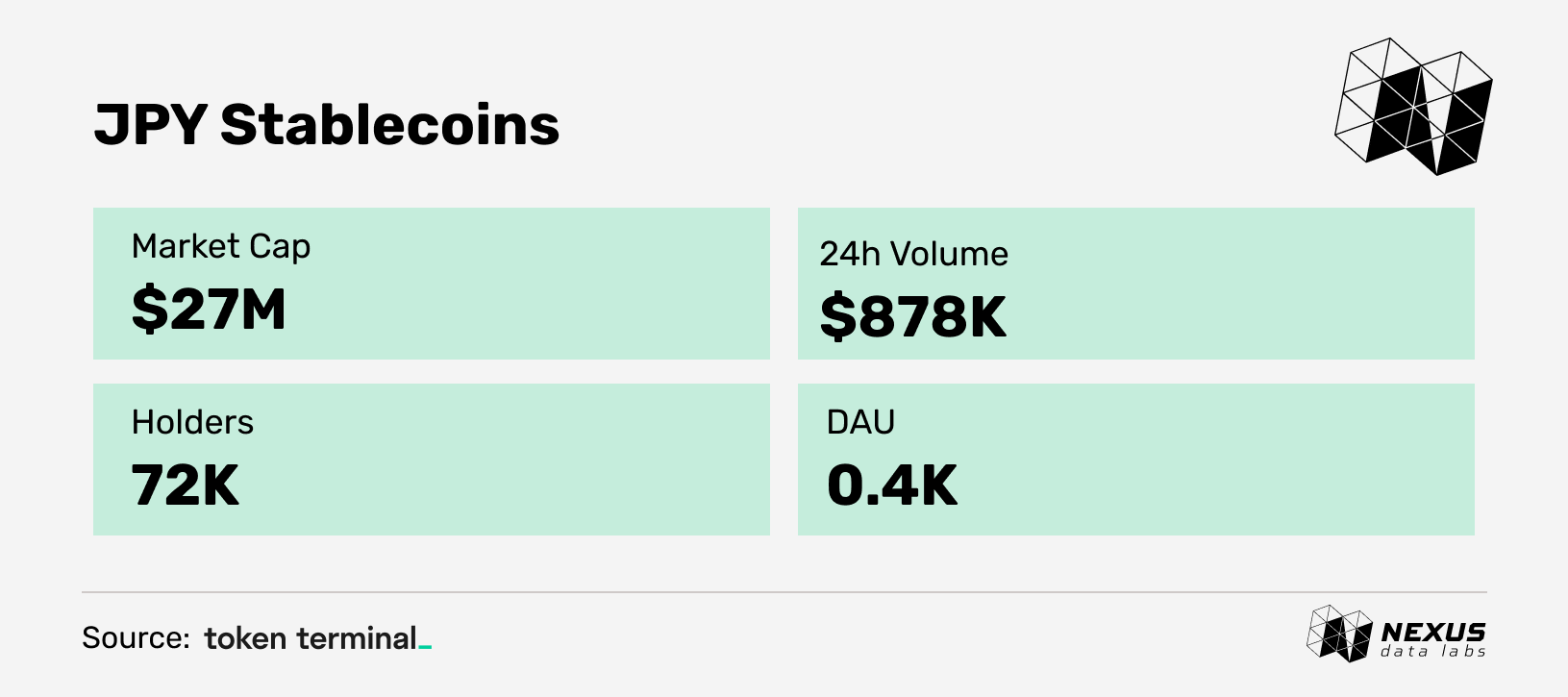

EURC accounts for the majority of that growth and remains the dominant non-USD stablecoin by both supply and volume. But growth has not been limited to a single asset or region. Brazilian real, Swiss franc, Japanese yen, and Singapore dollar stablecoins have all expanded in supply, each responding to local demand rather than a single macro catalyst. Three forces are driving this expansion: regulatory frameworks, a largely untapped addressable market, and a shifting competitive landscape.

The Regulatory Catalyst

The strongest structural driver of this growth has been regulatory clarity.

Circle’s EURC became the first MiCA-licensed euro stablecoin in July 2024. Post-MiCA, EURC volumes increased 1,139% and Societe Generale’s EURCV volumes rose 343%. Building on that momentum, a consortium of 12 European banks, including ING, UniCredit, BNP Paribas, and BBVA, formed Qivalis to launch a MiCA-compliant euro stablecoin in H2 2026.

Japan’s JPYC launched as the country’s first regulated yen-backed stablecoin in October 2025, registered under Japan’s Financial Services Agency.

South Korea saw KRW1 launch on Avalanche in September 2025 and KRWQ debut on Coinbase’s Base in October 2025. KakaoBank advanced its won-pegged stablecoin preparations ahead of pending legislation.

The pattern is clear: a wave of sovereign stablecoin issuance, with each jurisdiction effectively betting that its currency deserves a position in the onchain economy.

Market Size: The Opportunity in Context

The addressable market for non-USD stablecoins is significant regardless of how it is framed. Global M2 outside the United States is estimated around $100T, meaning even 1% stablecoin penetration implies an $800B to $1T opportunity.

Cross-border payment flows reached approximately $208T in 2025, projected to exceed $320T by 2032. B2B payments alone account for more than $34T annually. Remittance costs still average around 6.5%, largely driven by FX spreads and correspondent banking fees. These are the frictions that local currency stablecoins directly reduce.

Total non-USD stablecoin supply currently sits at approximately $1.29B, or 0.4% of the total stablecoin market. The gap between current supply and the implied opportunity speaks for itself. The constraint is not demand. It is infrastructure maturity, regulatory clarity, and distribution, and all three are progressing.

Current Market: The Dollar Network Effect

The primary competitor to non-USD stablecoins is the entrenched position of USD-denominated assets across every layer of the onchain economy.

USDT and USDC dominate liquidity on every major chain, DEX, and CEX. Most DeFi protocols are built around dollar-denominated collateral. Most traders price in dollars. Most crypto-native users hold dollars as their base asset.

This network effect is the single largest structural barrier to non-USD stablecoin adoption. Even users in countries with strong local currencies often default to USD stablecoins simply because liquidity is more readily available and integrations are established.

The implication: non-USD stablecoins will not win by competing with USDT or USDC head-on. They will win by serving the use cases where dollar denomination creates friction: domestic treasury operations, local payment rails, and regional B2B settlement. In these contexts, local currency is not a preference but a necessity.

The Protocols: Who Is Building

EURC is the largest non-USD stablecoin by supply and transfer volume. Issued by Circle, fully reserved, and MiCA-compliant, it has emerged as the dominant digital euro.

Frankencoin (ZCHF) is the largest CHF stablecoin onchain, pegged 1:1 to the Swiss franc. ZCHF's market cap reached $38M while average wallet balance declined from roughly $90K to under $25K.

BRZ by Transfero is the largest BRL-pegged stablecoin onchain, with $445M in circulating supply and over 8,600 holders.

Closing Thoughts

The structural gap between real-world FX and onchain is not permanent. It is a byproduct of how the stablecoin market was built, and the data indicates the gap is beginning to narrow.

The evidence over the past three years is consistent. The question is no longer whether this gap closes, but at what pace, and which protocols capture the most value in the process.

The non-USD stablecoin dashboard built in partnership with Token Terminal is designed to track this in real time, across every major non-USD stablecoin, with the full stack of onchain metrics that matter. The dashboard is a work in progress, and we welcome feedback as we continue to refine it. The opportunity is measured in trillions. The infrastructure to capture it is just getting started.