Nexus Opinion - The "Truth Machine" That Takes Your Money

The crowd does not produce the wisdom. The crowd is paying for it.

By Diego Cabral

The article is also available on X.

Setting the Scene

Kalshi CEO Tarek Mansour calls prediction markets “quintessential truth machines.” Polymarket CEO Shane Coplan goes further, calling his platform "the most accurate thing we have as mankind right now." These claims are bold, and the data largely supports them.

But accuracy is only half the story. The other half is about who actually produces it, who pays for it, and whether the "wisdom of the crowd" these platforms credit has anything to do with it.

The Accuracy Is Real

According to Alex McCullough's Dune dashboard, Polymarket is correct 90.4% of the time four hours before resolution. Twelve hours out: 81.2%. One day: 75.2%. One week: 78.3%. One month: 85.6%.

Raw accuracy is only part of the picture. The Brier score measures how closely a forecast matches reality, capturing not just whether it called the right side, but how confident it was. It runs from 0 (perfect) to 1 (perfectly wrong). Polymarket posted a Brier score of 0.0769 over the last two weeks. A coin-flip forecaster who calls everything 50/50 scores 0.25. Polymarket's 0.0769 is more than three times better, showing its prices usually carry real information, not only guesses.

The probabilities also align closely with reality. When Polymarket prices an event at 70%, it happens about 70% of the time. When it says 30%, the event happens about 30% of the time. That consistency is genuinely rare. Most forecasters, human or institutional, fail it.

As Andrew Courtney, a former derivatives trader and Good Judgment Project superforecaster, notes, the raw ‘N hours out’ accuracy figures are a coarse metric, tracking only whether markets priced above 50% resolved yes. The Brier score, the standard used in academic forecasting research, is more rigorous. It captures both confidence and precision, penalizing both errors and overconfidence.

The theory behind prediction market accuracy is decades old. Friedrich Hayek argued in 1945 that markets aggregate dispersed knowledge better than any central planner. Robin Hanson extended the idea in 2000, arguing markets could predict outcomes well enough to guide real decisions. In 2007, a group of economists including Nobel laureate Kenneth Arrow backed prediction markets as a serious forecasting tool.

The logic is simple. Give people with real information a financial incentive to act on it, and prices will reflect the truth.

The question is whether it works that way in practice, and who is actually behind the accuracy.

It Is Not the Crowd

The conventional answer points to the crowd.

Kalshi says its markets "leverage the wisdom of crowds," aggregating the knowledge and insights of a diverse group of participants. Polymarket attributes its edge to the "collective intelligence" of diverse traders. Both echo the Francis Galton story, where the averaged guesses of a crowd land closer to an ox's true weight than any individual expert.

The data tells a different story. A working paper published in April 2026 by researchers from London Business School and Yale University tested this claim directly using the full transaction history of Polymarket from January 2023 to December 2025, which covers 1.72M accounts and $13.76B in trading volume.

Their conclusion: prediction market “accuracy is driven by a small minority of informed traders.”

To separate skill from luck, the researchers developed a statistical test that randomizes the direction of each trader’s actual trades 10,000 times, generating a baseline of what random trading would have produced. Traders whose real profits significantly exceed that baseline are classified as genuinely skilled.

The result: only 3.1% of accounts are classified as skilled winners.

The rest break down as follows:

29.0% are lucky winners, with positive returns but no statistical evidence of skill

61.4% are unlucky losers

6.4% are unskilled losers, trading consistently in the wrong direction

0.1% are market makers

That 3.1% is not just a minority. It is what powers the entire “wisdom of the crowd.”

As a whole, the crowd adds noise, not real information.

This pattern is not unique to financial prediction markets. Research by the team behind the Good Judgment Project found the same structure in non-financial forecasting. A small elite of ‘superforecasters,’ selected purely by past accuracy, outperformed regular forecasters by roughly 60% on Brier scores. Their edge grew over time rather than regressing.

The informed minority is not unique to Polymarket. Academic evidence suggests the same structure appears across competitive forecasting environments.

Skill Persists

The same paper finds "an unusual degree of skill persistence in prediction markets." Among traders classified as skilled in one half of the data, 44% remained skilled in the other half. By comparison, skill in active mutual funds persists at just 10%, meaning prediction market skill is more than four times stickier than professional fund management.

This matters for what prediction market accuracy actually means. Prices are not accurate because thousands of small contributions cancel out the errors. They are accurate because a small, persistent group of skilled traders corrects mispricings and gets paid for doing so.

Who Pays for the “Truth”

If 3.1% of accounts generate the information, the remaining 96.9% provide something else: capital and volume.

An analysis by Andrey Sergeenkov, also covering the full trading history of all Polymarket addresses, puts a dollar figure on this dynamic. Sergeenkov calculated realized PnL across all USDC flows. The result: 84.1% of Polymarket traders lose money.

The concentration at the top is severe:

Only 2% of all 2.5M accounts have ever made more than $1K in lifetime profit

0.32%, roughly 8,000 addresses, have made more than $10K

0.03%, or 840 addresses, have made more than $100K

Monthly sustainability is even harder:

In any given month, fewer than 1% of accounts earn more than $5K

Two months in a row: 0.1%

Three consecutive months: 0.03%

Four months running: 0.015%

Among accounts that average more than $5K in profit per month, 53% achieved it in a single month only. Just 2.6% sustained it for longer than a year.

One important nuance matters here. Raw profit and genuine skill are not the same thing. The London Business School and Yale paper shows that among the top traders ranked by realized profits, only 12% overlap with the accounts statistically classified as skilled. Making money on Polymarket is not necessarily proof of skill. Many profitable accounts are simply lucky, and the data suggests that luck does not persist. Among traders classified as lucky winners in the first half of the data, 60% became losers in the subsequent period.

Most Volume Produces "Belief," not "Truth"

There is another dimension to this story, one that complicates the “truth machine” narrative further.

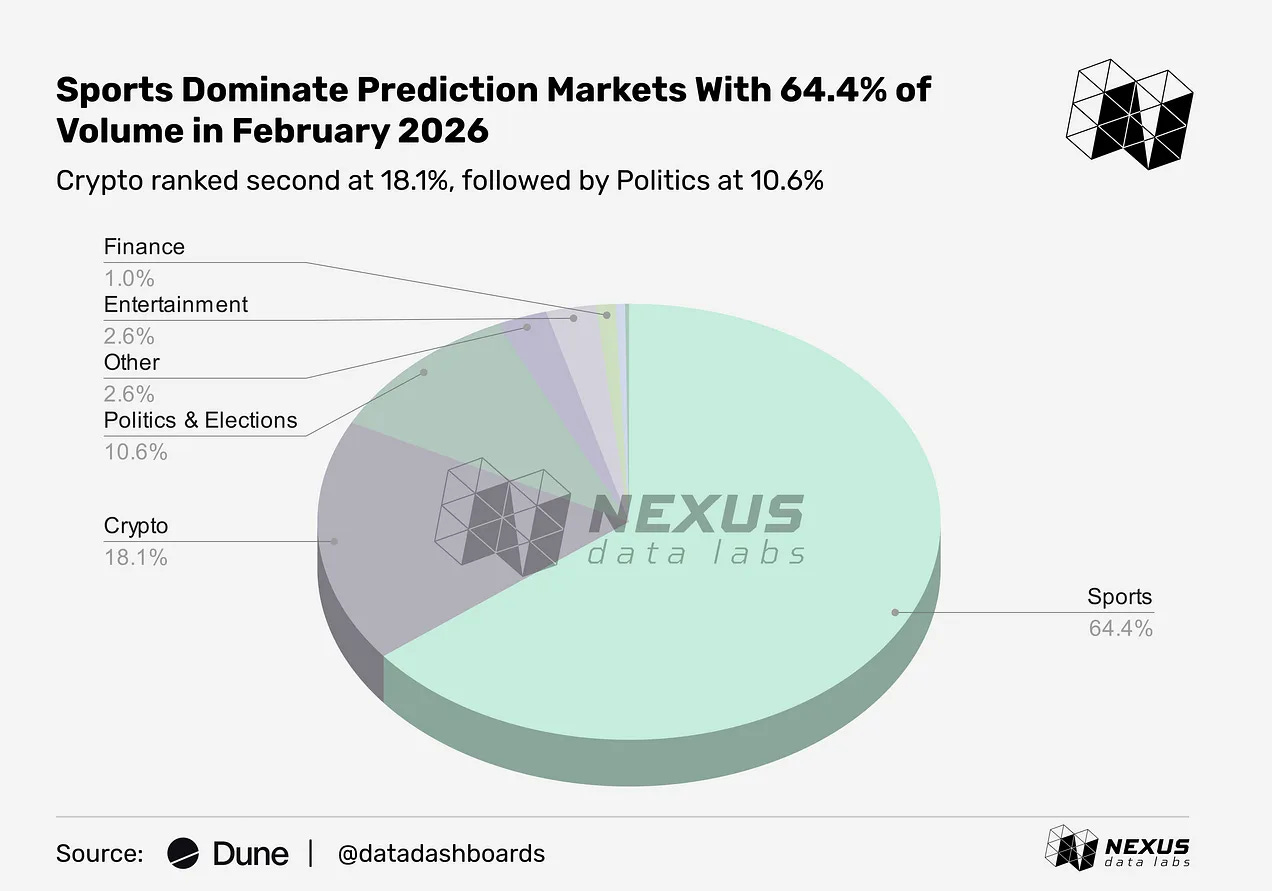

Dan Schwarz, former CTO of Metaculus, published an analysis of Kalshi and Polymarket. His finding: over 80% of Polymarket's trading volume is concentrated in sports, cryptocurrency prices, and election betting. On Kalshi, roughly 90% comes from sports alone.

This is consistent with what Nexus published in March 2026, where sports and crypto alone represented 82.5% of all volume in February 2026 on Kalshi and Polymarket combined.

The distinction matters. A sports bet or a crypto price market is not necessarily an attempt at truth-seeking, and it is not aggregating knowledge at all. It can simply represent a belief or preference expressed as a wager. In this scenario, the "truth machine" claim applies, at best, to the narrow slice of markets designed to inform decisions in the first place.

Schwarz defines "useful" markets as those with real potential to inform decisions: geopolitical risk monitoring, policy outcomes, accountability for public claims, interpreting economic news, and generating new information. After filtering out sports, crypto, and entertainment, he identifies roughly 6,800 markets as potentially valuable, out of approximately 194,000 across both platforms.

Among those useful markets, accuracy improved steadily through early 2025, then plateaued. Median volume per useful market has since declined, from a peak of $81K to $42K. For markets resolving in under 90 days, Schwarz finds no statistically significant relationship between trading volume and accuracy.

Some categories work as intended. Schwarz identifies geopolitical risk monitoring as an area where the markets work as advertised: nearly $3.8B in volume across 2,821 markets, increasingly cited by mainstream media. Still, the median useful market has experienced declining volume.

Schwarz concludes that the accuracy Polymarket advertises on its homepage is real, but concentrated in a narrow slice of markets that very few participants actually trade.

What the Data Tells Us

Comparing accuracy across platforms and categories is harder than it looks. Some markets are simply more predictable than others. A coin-flip market has no "wisdom" to aggregate regardless of who trades it. So a high accuracy score does not always mean skilled forecasting.

There is one more layer worth acknowledging. Prediction market contracts have a structural ambiguity problem that goes beyond question difficulty. Traders frequently do not fully understand what they are betting on, and resolution becomes a question of rule interpretation rather than “truth”. Anyone with a background in contract law will recognize the pattern. Vague drafting plus discretionary interpretation equals disputes. In prediction markets, that discretion sits with UMA token holders, a mechanism that remains contested.

With those caveats in mind, four independent datasets still point to the same conclusion.

McCullough's dashboard confirms Polymarket's forecasts are accurate.

Schwarz's analysis shows most volume sits in entertainment markets while useful-market accuracy has plateaued.

Sergeenkov's data shows 84.1% of traders lose money.

The London Business School and Yale paper identifies the mechanism: a persistently skilled 3% drives the real price discovery, while everyone else funds them.

None of this means the platforms are broken. The accuracy is real, and the markets work as designed. In specific domains, these markets produce genuine signal and deliver it faster than traditional forecasting.

But “truth machine” and “wisdom of the crowd” are a marketing claims.

The data says something more precise. Prediction markets are accurate forecasting tools for a narrow set of questions, built on a platform that operates primarily as a gambling product, where a small, persistently skilled minority extracts value from the majority who provide capital, volume, and noise.

A skilled minority of around 3% does the forecasting. A fraction of a percent earns a living from it. Everyone else funds them.

The crowd does not produce the wisdom. It finances the people who do.

What We're Watching

Web3 Data Jobs

Nexus is partnering with Unchain Data to highlight opportunities across the onchain data ecosystem. This week’s featured openings: