Nexus Data #010 - State of Tokenization Breakdown

A Nexus read on Pantera Capital's State of Tokenization report

Intro

Welcome to the tenth edition of Nexus Data Labs, where we highlight what matters most in the fast-developing world of onchain finance.

Thank you to J.W. and Diego for contributing to this issue.

We would also like to acknowledge the opportunity to have contributed a small part to Pantera Capital’s State of Tokenization report, and this week’s edition highlights a few of the most interesting data points and our take on them.

Setting the Scene

Tokenization is clearly scaling, but most tokenized assets are still wrappers. Pantera Capital's State of Tokenization report quantifies what the market has been sensing: the industry is moving in the right direction, but it has not yet demonstrated that onchain representation fundamentally changes how those assets function.

That aligns with Nexus’s historical view: RWAs need to become more than simple representations of assets held offchain. Without active integration with DeFi, tokenized assets risk becoming little more than mirrored ledgers.

This week, Nexus unpacks Pantera Capital’s Tokenization Progress Index (TPI) and highlights a few of the data points that stood out in the report. For the full narrative and underlying methodology, see the full report on State of Tokenization.

Tokenization Progress Index (TPI)

The tokenized asset universe scores 2.04 out of 5 on onchain maturity

The Tokenization Progress Index (TPI) is Pantera Capital’s framework for measuring how far a tokenized asset has progressed onchain. It scores each asset across three dimensions, each rated from 1 to 5:

Issuance & Redemption: how assets are minted and redeemed

Transferability & Settlement: how assets transfer and settle

Complexity & Composability: how assets can be deployed in smart contracts

The composite TPI score is the average of those three dimensions. Assets are then bucketed into three tiers:

Wrappers: onchain representations of offchain claims (TPI of 2.5 or below)

Hybrids: assets with partial onchain functionality (TPI above 2.5 and below 3.5)

Natives: assets designed to operate primarily onchain (TPI of 3.5 or above)

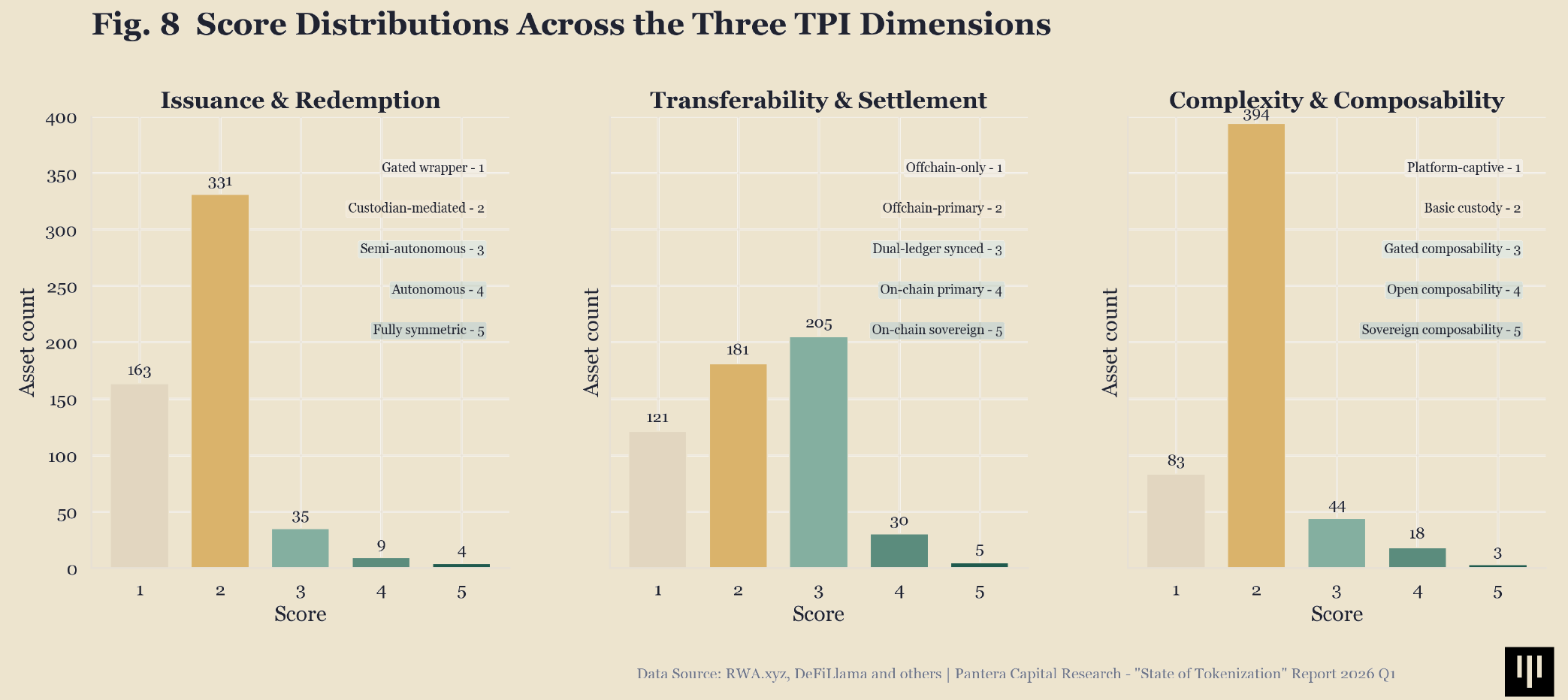

Per Pantera Capital’s scoring, the market averages just 2.04 out of 5 across scored assets. Wrappers account for 77.6% of the universe, Hybrids 11.1%, and Natives only 2.7%. Of the three dimensions, Transferability & Settlement has progressed the furthest, with 44.3% of assets reaching a score of 3 or higher. Issuance & Redemption and Complexity & Composability both lag, with roughly 90% of scored assets remaining at scores of 1 or 2 in each dimension.

Transfer and settlement are the first dimension showing progress, while the other two still have significant ground to cover. For the market to move beyond wrappers, onchain transferability alone is not enough. The takeaway from the TPI data is clear: tokenization has proven that assets can be represented onchain, but it has not yet proven they can operate natively there.

Tokenization Market = Stablecoin Market

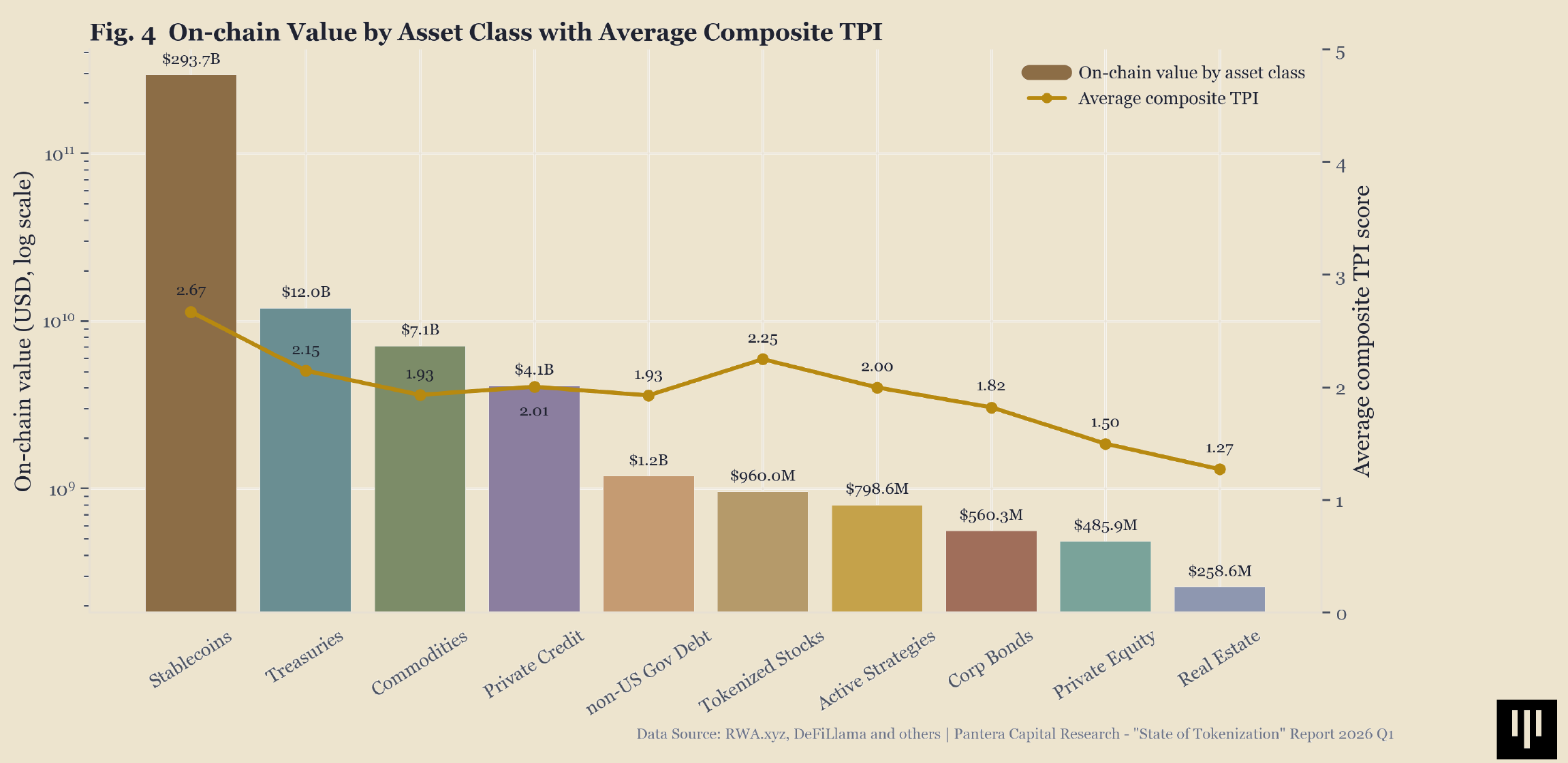

Stablecoins account for 91.6% of all tokenized assets

Stablecoins make up 91.6% of total tokenized market value. Every other asset class, including Treasuries, Commodities, and Private Credit, fits inside the remaining 8.4%. In other words, most tokenization growth charts are stablecoin charts in disguise at the moment.

The gap is not just about size. Stablecoins also have the highest average composite TPI at 2.67, ahead of every other asset class. Most other categories cluster around or below 2:

Treasuries: 2.15

Commodities: 1.93

Private Credit: 2.01

Real Estate: 1.27

Removing stablecoins reveals a much smaller and earlier market. Tokenized Treasuries at $12B and Commodities at $7B lead the remaining categories, but neither approaches the scale or maturity of stablecoins. Until other asset classes scale meaningfully, tokenization’s headline numbers will continue to be dominated by a single category.

Capital and Maturity: A Chicken-or-Egg Problem

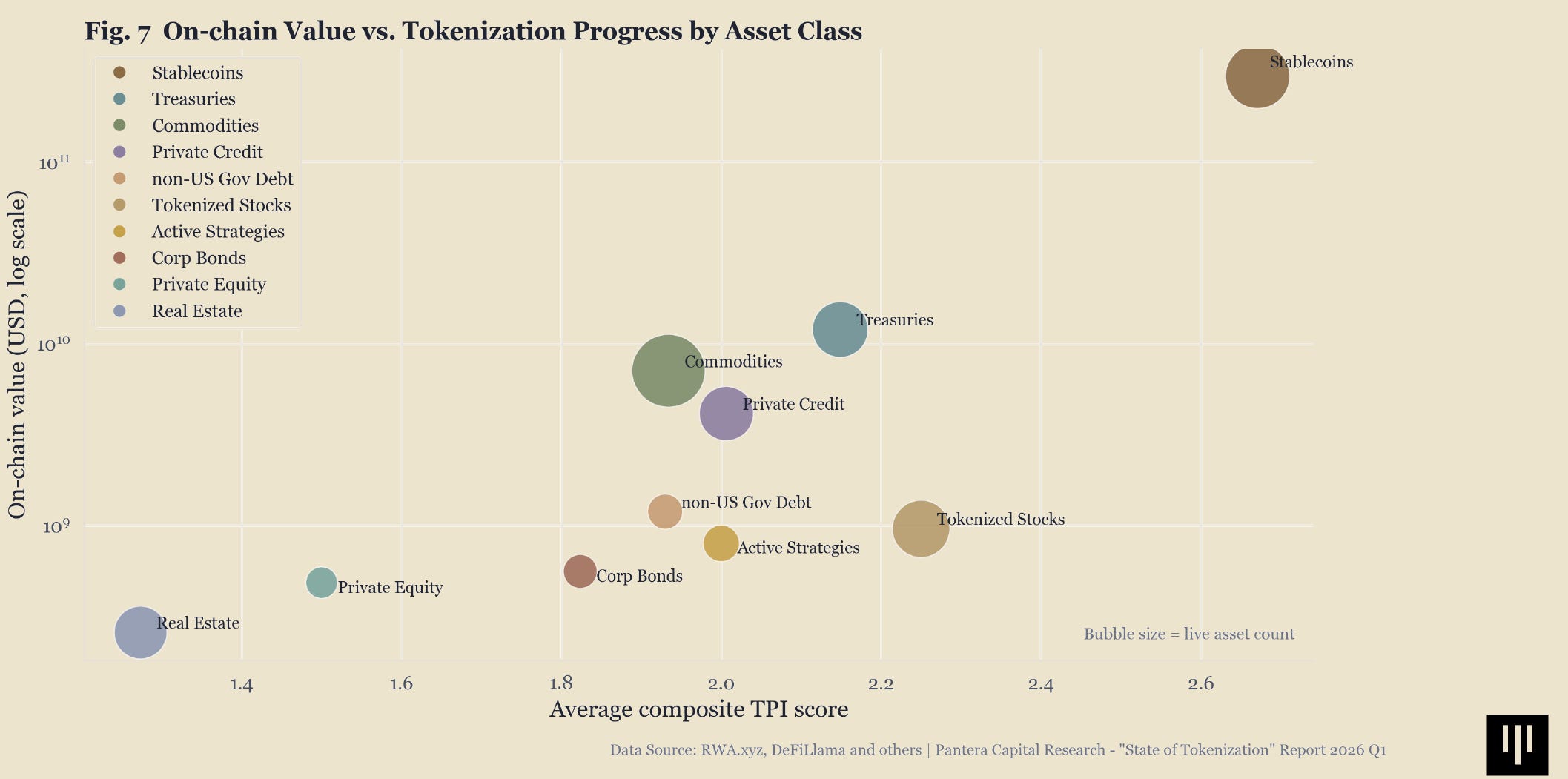

Capital and maturity are moving together, but which leads is still unclear

At the asset-class level, the categories with the most capital onchain also tend to score higher on maturity. Stablecoins lead both dimensions at $293B and a TPI of 2.67. Treasuries follow at $12B and 2.15. Beyond that, market value generally declines alongside TPI.

Tokenized Stocks are a notable outlier at $960M and a TPI of 2.25, ahead of categories with significantly more capital. The underlying assets are simpler than other tokenized categories: high liquidity, real-time price feeds, and standardized settlement. That structural simplicity gives tokenized equities an advantage in onchain maturity.

Real Estate ($259M, TPI 1.27) and Private Equity ($486M, TPI 1.50) sit at the opposite end. Both rely on illiquid underlying assets, complex legal structures, and valuation processes that still run entirely offchain. Those characteristics make them the hardest categories to move beyond the wrapper phase.

Asset complexity appears to be related to tokenization maturity. Liquid, standardized assets tend to progress faster onchain, while more complex and illiquid categories lag. The market is beginning to reflect that pattern, but most asset classes still cluster in the lower-middle range of TPI.

There is a chicken-or-egg dynamic at play. Does higher onchain maturity attract capital, or does capital inflow fund the infrastructure that raises maturity? It is difficult to say which leads, but the data shows that scale and maturity are beginning to move in the same direction.

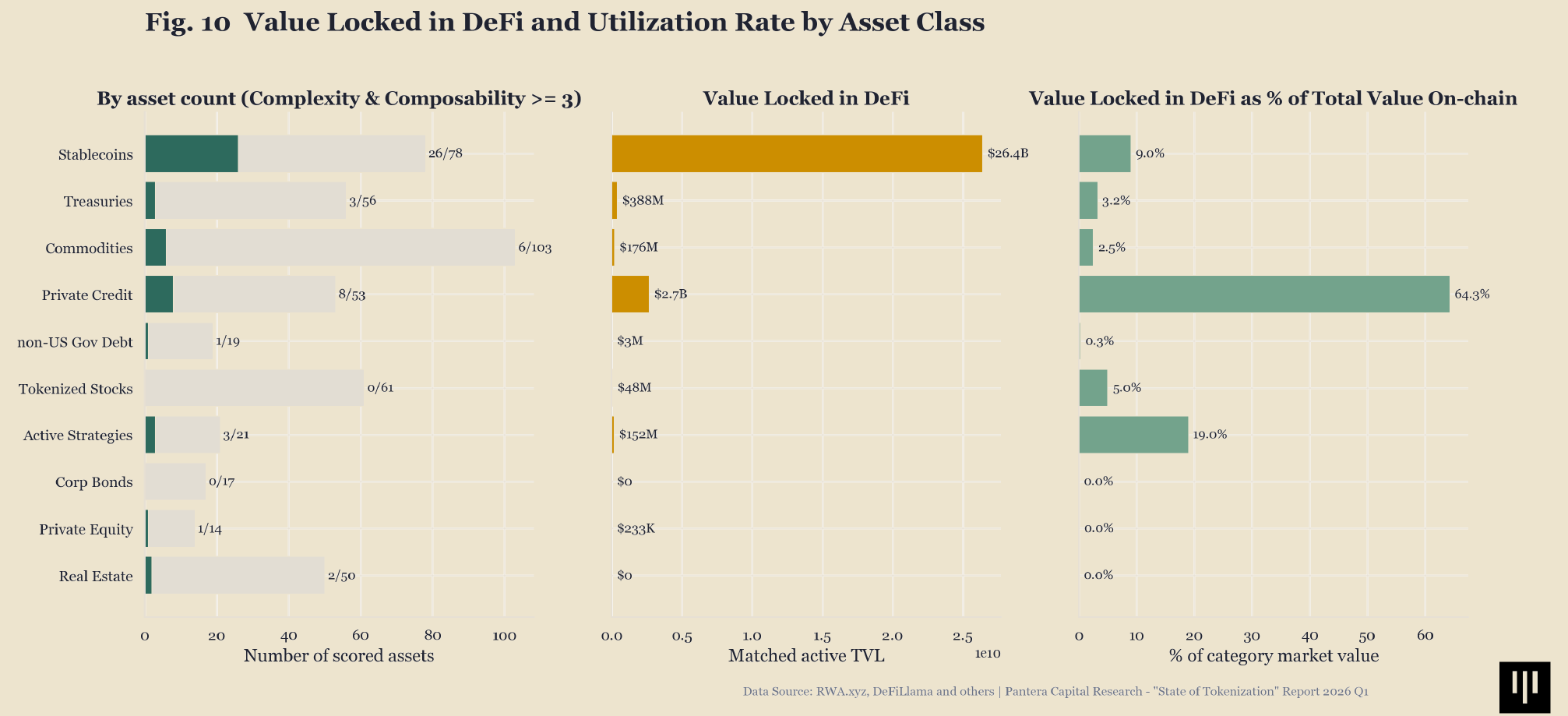

Private Credit Leads DeFi Utilization

64.3% of tokenized Private Credit is deployed in DeFi, compared to 9.0% for stablecoins

The most notable finding in the report is not about size. It is about utility. Of all tokenized Private Credit onchain, 64.3% is actively utilized in DeFi protocols. Stablecoins, despite being the largest category by far, sit at just 9.0%. On a utilization basis, Private Credit is the most onchain-active asset class in the tokenized universe.

That number comes with a caveat. Private Credit's DeFi usage is concentrated in a small number of products. Maple's syrupUSDT and syrupUSDC together account for approximately two-thirds of the category's active DeFi TVL. A similar concentration appears in Active Strategies, where 19% of the category's value is locked in DeFi, but Superstate's Crypto Carry Fund alone accounts for approximately 80% of that total.

Composability exists in both cases, but it has not yet broadened across the category. A small number of protocols are proving that tokenized assets can be productive onchain. When a tokenized asset is designed for DeFi composability, utilization follows. The challenge is extending that design pattern to more asset classes. Until that happens, composability will remain concentrated in the few categories and projects built for it.

Closing Thoughts

Tokenization is scaling. Maturity is not, at least not at the same pace. A TPI average of 2.04 out of 5 and a Wrapper share of 77.6% confirm that most tokenized assets now exist onchain in form, but not yet in function. That is an important first step, but it is not the final destination.

The market has proven that assets can be represented onchain. What it has not yet proven is that onchain representation changes how those assets actually work. Issuance remains gated, redemption routes through custodians, and composability is concentrated in stablecoins and a handful of private credit products. For most of the market, the token is moving onchain while the asset’s actual lifecycle remains anchored offchain. The market is heading in the right direction, but most of the work is still ahead.

Tokenization was never the endgame. Integrating those assets into the onchain economy is. The industry needs to move past replicating offchain products on a new ledger and start designing for what blockchains make uniquely possible. The tokenized market is still early. Whether it matures beyond the wrapper phase depends on whether the next wave of issuance is built for onchain utility, not just onchain presence.

What We're Watching

A Data-Driven Guide to Blockchain Infrastructure for TradFi Tokenization

Mapping Contagion and Counterparties in the Sea of Tokens and Protocols

Web3 Data Jobs

Nexus is partnering with Unchain Data to highlight opportunities across the onchain data ecosystem. This week’s featured openings: