Nexus Data #011 - The Great L2 Migration That Never Happened

A deep dive into onchain activity across Ethereum mainnet and L2s.

Intro

In November 2025, Vitalik responded to an X post noting that Ethereum L1 fees had been negligible all year. His take was simple: just build on L1. He doubled down in February 2026, stating that Ethereum’s L2 scaling roadmap “no longer makes sense.” Both statements raise a question: is activity migrating back to Ethereum mainnet?

To answer that, this analysis examines three high-level metrics that capture the broadest view of network activity: revenue, transaction count, and total value secured (TVS). These are not the only metrics that matter, and other metrics such as DEX volumes or contract deployments may surface different patterns. But revenue, transactions, and TVS represent the foundational indicators that most market participants use to assess where activity lives. If migration were happening at any meaningful scale, it would show up there first.

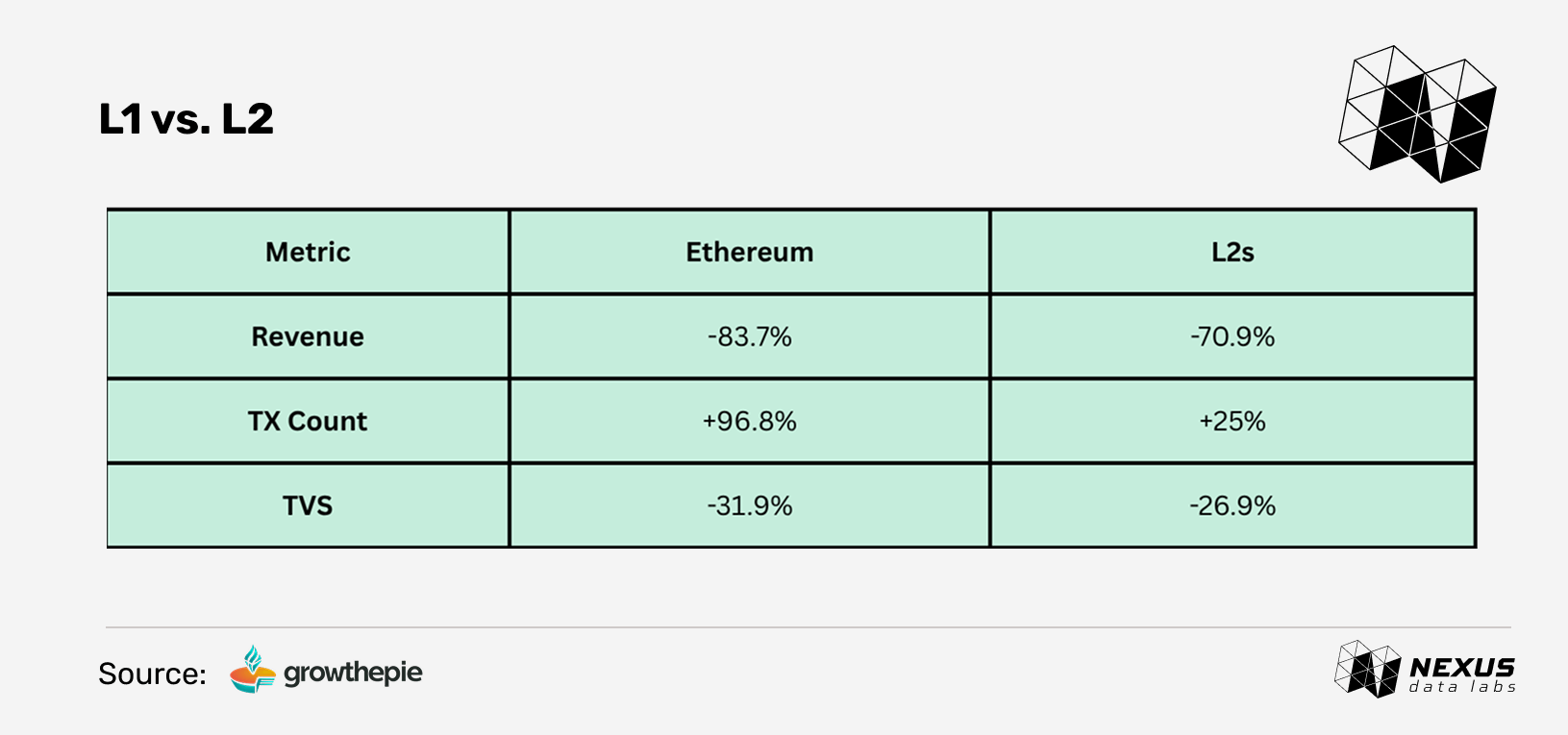

Revenue: An Ecosystem-Wide Collapse

Ethereum mainnet revenue collapsed from $147M per month in January 2025 to $24M per month in April 2026. L2 revenue followed a similar trajectory, dropping from $22M per month to $6M per month over the same period. Both L1 and L2 fees compressed sharply in early 2025 and have remained at relatively low levels since.

However, revenue alone does not tell us whether usage migrated. Lower revenue can reflect lower fees, not necessarily lower activity. In this case, the decline appears to be driven primarily by a combination of weaker ETH prices, persistently low gas costs, and a broader cooling in speculative activity. Ethereum mainnet still generates materially more revenue than the combined L2 set, and the decline in fees is better understood as a market-wide compression than as evidence of a structural shift from L2s back to L1.

Transactions: Growth Without Migration

Transaction count gives a cleaner view of usage than revenue. On Ethereum mainnet, monthly transactions rose from 37M in early 2025 to 73M in April 2026, nearly doubling over 15 months. Combined L2 transactions stayed broadly stable in the 0.8B to 1.0B range over the same period.

There is, however, a notable distortion in the recent L2 data: the launch of MegaETH produced a temporary spike in L2 transaction counts that has since normalized. Excluding that, mainnet transaction count is growing while L2 transaction count has largely held steady. Even so, the aggregate L2 figure deserves scrutiny. New L2s continuously launch with incentive programs that attract bot activity and wash trading, inflating transaction counts before those chains fade to near-zero usage. The combined L2 number likely overstates organic activity.

The scale difference adds context. L2 transaction counts run in the hundreds of millions to billions per month, roughly 20x Ethereum mainnet. A gain of 30M monthly transactions is meaningful for mainnet. On the L2 side, that same volume is a rounding error. Mainnet’s transaction growth, while meaningful in isolation, does not constitute evidence of migration unless it is accompanied by a corresponding decline on the L2 side, which has not materialized.

TVS: L2s Are Holding Up, but Everything Is Down

Total value secured on both Ethereum mainnet and L2s rose through mid-2025 and has trended lower since. Ethereum reached $91B in August 2025, while L2s hit $53B in September 2025. Neither has returned to those levels.

Since January 2025, Ethereum mainnet TVS has declined from $66B to $45B, a decline of 31.9%. L2 TVS has dropped from $52B to $38B, or 26.9%, over the same period. The divergence is more noticeable in 2026: Ethereum is down 31.7% YTD, compared to “only” 11.4% for L2s.

These moves are still largely tied to ETH price. As ETH falls in dollar terms, so do dollar-denominated TVS figures. L2s have held up somewhat better than mainnet in percentage terms, but the broader trend is the same across both layers: both ecosystems are contracting in USD terms. That points to a market-wide drawdown rather than a reallocation of capital from L2s back to Ethereum mainnet.

The Bifurcation Inside L2s

The more interesting story is not between L1 and L2, but within L2s themselves. Among the top five L2s by TVL, only Base and Polygon have posted positive TVL growth YTD, at +2% and +6% respectively. Arbitrum is down 6%, Mantle is down 14%, and Optimism is down 28%.

The difference comes down to demand quality. The chains holding up have durable sources of activity that do not rely entirely on incentive cycles. Base benefits from Coinbase distribution, has no token, and has several major native applications including Aerodrome, Limitless, and Bankr. Polygon has Polymarket, which creates significant and persistent demand for blockspace. By contrast, the weaker chains have not built the same kind of structural moat. Arbitrum has the broadest app diversity but no dominant anchor application. Optimism onboarded EtherFi Cash in April 2026 and still posted a -28% TVL decline YTD.

This pattern also appears at the ecosystem level. GrowThePie tracks 97 live L2s above the $100K TVS threshold, down from 109 in June 2025. Many of these chains launched with incentive programs and now sit with near-zero activity. L2s are not losing users to Ethereum mainnet. Once incentive programs end, users simply move on to the next one.

Editor’s Note: GrowThePie tracks nearly 150 L2s in total. The figures above only include chains above the $100K TVS threshold. As ETH prices decline, some chains can fall below this cutoff without actually shutting down, so the true number of active L2s is likely higher than 97.

The (Lack of) Application Diversity

Application diversity is the clearest sign of L2 resilience. Ethereum mainnet hosts a broad mix of activity across lending, staking, DeFi, NFT infrastructure, and other categories. DeFiLlama tracks 1,863 protocols on Ethereum mainnet, followed by BSC (1,158), Arbitrum (1,117), and Base (948).

Among the top L2s, Arbitrum and Base are building toward broader diversification. The others are more concentrated. Polygon is heavily shaped by Polymarket, Optimism by EtherFi, and Mantle by Aave. That concentration can be a strength when the anchor application is growing. It can also be a weakness when the anchor slows, shifts chain strategy, or loses share.

Polymarket is the clearest example. On February 9, 2026, Polymarket demand pushed Polygon transaction costs higher than Ethereum mainnet’s, not because Polygon failed to scale, but because its blockspace was valuable enough that users were willing to pay a premium for it.

But concentration cuts both ways. When a chain’s activity depends primarily on one protocol, its trajectory becomes tied to that team’s decisions. If that application migrates to another chain, slows down, or pivots its product, the network’s metrics follow. Nexus explored this dynamic in a previous analysis of Polymarket within Polygon. Chains with diverse ecosystems can absorb those shocks more easily. Chains built around a single application inherit its risks.

Is the Migration Happening?

Across the three metrics examined, the data does not provide strong evidence of a broad migration from L2s back to Ethereum mainnet. Revenue and TVS are both down across L1 and L2s, driven by ETH price declines and fee compression rather than a structural shift in where users are transacting. Mainnet transaction count nearly doubled, which is notable, but without a corresponding decline on the L2 side, it is difficult to attribute that growth to migration rather than organic expansion.

What the data does reveal clearly is something more consequential: a consolidation within the L2 landscape itself. Activity is not flowing back to Ethereum mainnet. It is concentrating into the few L2s that built durable demand sources, while the rest fade after incentive programs end.

Vitalik’s recent comments should be read in that context. They were not a call for everyone to return to mainnet. They were a recognition that generic rollups serving only as cheap blockspace extensions may no longer be the right long-term answer. A recent Galaxy Research analysis of the Strawmap frames this as an explicit course correction away from the rollup-centric approach that defined the 2022–2025 cycle, with the direction now to scale the base layer, close the usage gap, and reduce dependency on L2s as the primary throughput solution.

The result is not a return to a pure L1 world. It is a pruning of the L2 stack. Most L2s are not losing users to Ethereum mainnet. They are losing relevance because they never developed enough independent demand to survive beyond the incentive cycle.

Methodology

The L2 data in the transaction count and TVS charts includes the following chains: Arbitrum One, Arbitrum Nova, Base, Celo, Fraxtal, Gravity, Ink, Linea, Loopring, Manta Pacific, Mantle, MegaETH, Metis, Mode Network, Optimism, Plume Network, Polygon, Ronin, Scroll, Soneium, Starknet, Taiko Alethia, Unichain, World Chain, and ZKsync Era.

What We're Watching

Web3 Data Jobs

Nexus is partnering with Unchain Data to highlight opportunities across the onchain data ecosystem. This week’s featured openings: